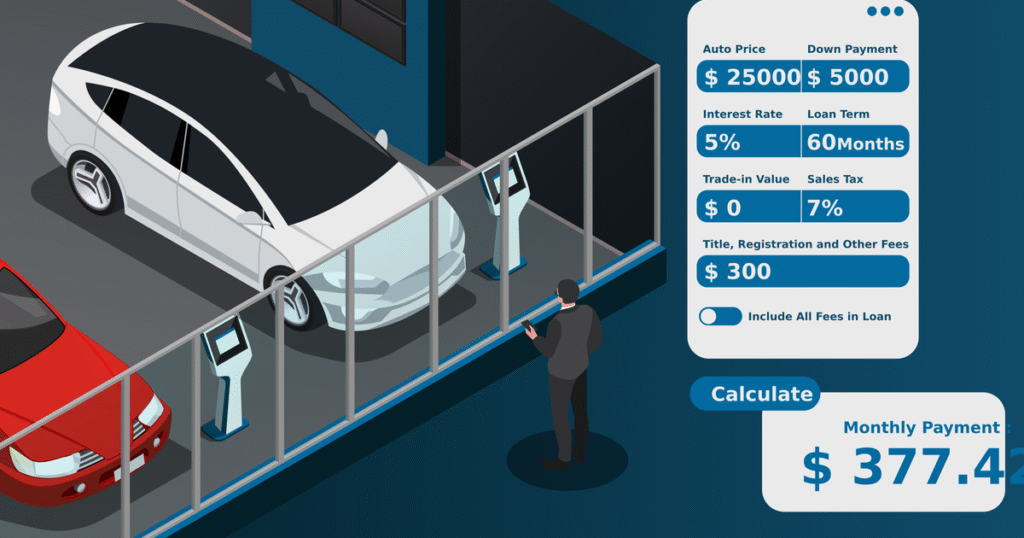

Car Loan Calculator

Loan Summary

Loan Amount: $0

Monthly Payment: $0

Total Interest: $0

Total Cost: $0

Amortization Schedule

| Month | Payment | Principal | Interest | Balance |

|---|

Beyond the Monthly Payment: The Ultimate Guide to the Car Loan Calculator

The scent of a new car is intoxicating. The gleam of polished paint under the showroom lights, the feel of a brand-new steering wheel, the promise of open roads and newfound freedom—it’s a potent combination. The American love affair with the automobile is as strong as ever.

But standing between you and that dream drive is a formidable gatekeeper: the finance office.

Suddenly, the conversation shifts from horsepower and trim levels to APRs, loan terms, and down payments. A friendly salesperson starts talking about an “easy low monthly payment,” and your head begins to spin. It’s a high-pressure environment designed to be confusing, a place where financial decisions worth tens of thousands of dollars are often made in a matter of minutes.

What if you could walk into that dealership armed with a secret weapon? A tool that cuts through the sales talk, demystifies the numbers, and puts you firmly in the driver’s seat of the negotiation?

That weapon is the car loan calculator.

And this isn’t just a guide on how to plug in numbers. This is your masterclass. We are going to dissect this essential tool, explore its every function, and teach you how to wield it to save thousands of dollars, avoid common traps, and drive off the lot with a deal you understand and a car you love. By the time you’re done reading, the car loan calculator will be your trusted co-pilot on the entire car-buying journey.

Chapter 1: The “Why” – What a Car Loan Calculator Really Is

On the surface, a car loan calculator is a simple tool: you input a few variables, and it tells you your estimated monthly payment. But to see it that way is like saying a smartphone is just a device for making calls. The true power lies in what it enables you to do.

A car loan calculator is a financial simulator for your next vehicle. It’s a risk-free environment where you can:

- Test-drive different budgets: See exactly how a $25,000 car compares to a $35,000 one in real-world monthly costs and total expense.

- Battle-test loan terms: Instantly visualize the massive difference in total interest paid between a 48-month loan and a 72-month loan.

- Expose the “monthly payment” trap: This is its most critical function. Dealers love to focus on the monthly payment because it’s easy to manipulate. By extending the loan term, they can make an expensive car seem affordable. The calculator reveals the devastating truth: a lower monthly payment over a longer term almost always means you pay thousands more in interest.

- Become a negotiation powerhouse: When you know your numbers cold, you can’t be easily swayed. You can confidently counter offers and spot a bad deal from a mile away.

In short, the calculator transforms you from a passenger being taken for a ride into the driver who sets the destination.

Chapter 2: The Anatomy of a Car Loan Calculator: Mastering the Inputs

A calculator is only as smart as the information you provide. Let’s break down every single input field you’ll encounter and how to use it with precision. We’ll follow a fictional buyer, Chloe, who is looking to buy her first new, reliable car.

1. Vehicle Price (The “Out-the-Door” Goal)

This seems simple, but it’s the first place buyers make a mistake. The number you should aim to use here is NOT the Manufacturer’s Suggested Retail Price (MSRP) you see on the window sticker. It’s the “Out-the-Door” (OTD) price.

- What it is: The OTD price is the total, final cost of the car. It includes the negotiated price of the vehicle, all taxes, and all mandatory fees (like documentation, title, and registration).

- Why it’s crucial: If you only calculate based on the vehicle’s price, you’ll be shocked when the final bill is thousands of dollars higher due to taxes and fees. Calculating with the OTD price gives you the most accurate picture of your loan amount and payment.

- How to use it: When you’re just starting, you can estimate. A good rule of thumb is to take the car’s list price and add about 10% to cover taxes and fees (this varies by state, but it’s a safe starting point for simulations). When you are seriously negotiating with a dealer, you should always ask for the OTD price sheet.

Example: Chloe is interested in a car with an MSRP of

28,000.Forherinitialcalculations,sheestimatesanOTDpriceofroughly∗∗28,000. For her initial calculations, she estimates an OTD price of roughly **28,000.Forherinitialcalculations,sheestimatesanOTDpriceofroughly∗∗

30,800* ($28,000 + 10%). This is the number she’ll start with in the calculator.*

2. Down Payment (Your First Move)

Your down payment is the cash you pay upfront. It reduces the amount you need to finance.

- What it is: A lump-sum cash payment (or the value of your trade-in) that you contribute at the time of purchase.

- Why it’s a power move:

- Reduces Your Loan: Every dollar you put down is a dollar you don’t have to pay interest on.

- Builds Instant Equity: Cars depreciate the second you drive them off the lot. A significant down payment helps you stay “right-side up” on your loan, meaning you owe less than the car is worth.

- Lowers Your Payment: A larger down payment directly leads to a smaller, more manageable monthly payment.

- Improves Approval Odds: It shows the lender you have skin in the game, which can lead to better interest rates.

- The 20/4/10 Rule: A popular financial guideline for car buying suggests:

- Put 20% down.

- Finance for no more than 4 years (48 months).

- Keep your total monthly car payment (including insurance and gas) under 10% of your gross monthly income.

- How to use it: Enter the total cash amount you’re comfortable putting down.

Example: Chloe has saved diligently and has $6,000 for a down payment. This is just under 20% of her estimated OTD price, a very strong start.

3. Trade-in Value (Your Bargaining Chip)

If you have a car to trade in, its value acts as part of your down payment.

- What it is: The amount a dealership offers you for your old vehicle.

- The Critical Step: Before you ever step foot in a dealership, you must research your trade-in’s value. Use online resources like Kelley Blue Book (KBB), Edmunds, and NADAGuides. Get quotes from online retailers like Carvana and Vroom. This gives you a baseline.

- Pro Tip: Always negotiate the price of the new car first, as if you don’t have a trade-in. Once you’ve agreed on a price, then introduce the trade-in. This prevents the dealer from “hiding” a low trade-in offer by giving you a slightly better price on the new car.

- How to use it: Add the realistic value of your trade-in to your cash down payment.

Example: Chloe doesn’t have a trade-in, so her value here is $0. Her total down payment remains $6,000.

4. Loan Term (The Interest Amplifier)

This is the length of your loan, usually expressed in months (e.g., 36, 48, 60, 72, 84). This is one of the most dangerous variables in the equation.

- The Seduction of Long Terms: Dealers love to offer 72-month (6-year) or even 84-month (7-year) loans. Why? Because it drastically lowers the monthly payment, making expensive cars seem affordable.

- The Harsh Reality:

- Interest Explosion: The longer the term, the more interest you pay. The difference between a 48-month and a 72-month loan can be thousands of dollars.

- Negative Equity: Cars depreciate fast. On a long-term loan, you’ll likely be “underwater” (owe more than the car is worth) for years. If the car is totaled or you need to sell it, you’ll have to write a check to the lender just to get rid of it.

- Outliving the Warranty: You could still be making payments long after the manufacturer’s warranty has expired, forcing you to pay for both a car note and expensive repairs.

- How to use it: Use the calculator to run a direct comparison. See the total cost difference between a 48-month and a 72-month loan. The results will shock you and solidify your resolve to stick with a shorter term.

Example: Chloe is disciplined and wants to follow the 20/4/10 rule as closely as possible. She decides to run her initial calculation using a 48-month term.

5. Interest Rate / APR (The Cost of Credit)

The Annual Percentage Rate (APR) is the price you pay for borrowing money. It includes the interest rate plus any lender fees.

- What influences it? Your credit score is the single biggest factor. A score of 760+ will command the best rates, while a score below 660 will result in much higher, subprime rates. The loan term also affects it (shorter terms often have lower rates).

- The Golden Rule: Get Pre-Approved! Before you shop for a car, you should shop for a loan. Apply for a car loan at your local credit union or bank. They will pre-approve you for a certain amount at a specific interest rate. This pre-approval is your trump card.

- It tells you what you can actually afford.

- It gives you a baseline rate to compare against the dealership’s financing offer. You can ask them, “Can you beat this rate?”

- How to use it: If you’re pre-approved, use that rate. If you’re just starting, use an online estimator based on your credit score tier (e.g., Excellent, Good, Fair, Poor).

Example: Chloe has a good credit score of 750. She got pre-approved by her credit union for an APR of 5.5% on a 48-month loan.

6. Sales Tax, Title, and Fees (The Non-Negotiables)

These are the costs that transform a vehicle price into an OTD price.

- Sales Tax: Varies by state, county, and even city. You can easily find your local rate online. It’s calculated on the taxable portion of the vehicle’s price.

- Documentation Fee (“Doc Fee”): A fee dealers charge for processing paperwork. This can range from under $100 to over $1,000. Some states cap it, others don’t. While often not negotiable, knowing the typical fee in your area helps you spot an excessive one.

- Title and Registration: The fees your state’s DMV charges to put the car in your name and give you license plates.

- How to use it: The best calculators have separate fields for these. If yours doesn’t, you must calculate them manually and add them to the vehicle price to get your true OTD loan amount.

Example: Chloe’s state has a 7% sales tax. On the $28,000 car, that’s $1,960. The dealer has a $499 doc fee, and title/registration is estimated at $350. Total taxes/fees = $2,809. So, her OTD price is $28,000 + $2,809 = $30,809. Her loan amount will be $30,809 –

6,000downpayment=∗∗6,000 down payment = **6,000downpayment=∗∗

24,809*.*

RECAP: Chloe’s Inputs

- Loan Amount: $24,809

- Loan Term: 48 months

- Interest Rate (APR): 5.5%

Now, let’s hit “Calculate” and see what the simulator tells us.

Chapter 3: Decoding the Results: Understanding the Outputs

The calculator’s output is more than just a monthly payment. It’s a complete financial story of your loan. Here’s how to read it.

1. The Monthly Payment

This is the number everyone focuses on. It’s the amount that will come out of your bank account every month.

For Chloe’s scenario, the calculated monthly payment is approximately $577.

This gives her a clear, tangible number to fit into her monthly budget.

2. The Amortization Schedule (The Financial X-Ray)

This is the most revealing part of the calculator. The amortization schedule is a table that shows a payment-by-payment breakdown of your loan. It typically has columns for: Payment Number, Principal Paid, Interest Paid, and Remaining Balance.

Here’s what Chloe would see for her first few payments:

| Payment # | Monthly Payment | Principal Paid | Interest Paid | Remaining Balance |

| 1 | $577 | $463.50 | $113.71 | $24,345.50 |

| 2 | $577 | $465.62 | $111.38 | $23,879.88 |

| 3 | $577 | $467.76 | $109.24 | $23,412.12 |

The Shocking Insight: Notice how in the beginning, a significant portion of her payment ($113.71 in the first month!) goes straight to interest. As the loan progresses, more of the payment shifts toward paying down the principal. This front-loading of interest is why long-term loans are so profitable for lenders and so costly for borrowers.

3. Total Interest Paid (The True Cost of Borrowing)

This is the “ouch” number. It’s the total amount of money you are paying the lender for the privilege of borrowing their money. It is pure cost, with no contribution to the value of your car.

For Chloe’s 48-month loan, the total interest paid would be approximately $2,887.

4. Total Cost of the Loan

This number sums up all of your monthly payments over the entire term. It’s the loan amount plus the total interest.

For Chloe, this would be $24,809 (Principal) +

2,887(Interest)=∗∗2,887 (Interest) = **2,887(Interest)=∗∗

27,696*.*

5. The Grand Total: The Real Price of the Car

To find the true, all-in cost of the vehicle, you add your down payment back to the total cost of the loan.

For Chloe, this is $27,696 (Total Payments) +

6,000(DownPayment)=∗∗6,000 (Down Payment) = **6,000(DownPayment)=∗∗

33,696*.*

This is a powerful moment of clarity. The car that started with a $28,000 sticker price will ultimately cost Chloe nearly $34,000 when all is said and done. The calculator makes this final, true cost transparent.

Chapter 4: Advanced Strategies: From Calculator User to Financial Pro

Now let’s put our tool to work and run some strategic simulations.

Strategy 1: The 48-Month vs. 72-Month War Games

The dealer tells Chloe, “I can get you into this car for just $410 a month!” That sounds amazing compared to $577. But how do they do it? They extend her loan to 72 months and, because it’s a longer term, her interest rate bumps up to 6.0%.

Let’s run the numbers in the calculator:

| Feature | 48-Month Loan @ 5.5% | 72-Month Loan @ 6.0% | Difference |

| Monthly Payment | $577 | $410 | -$167/month (Seems good!) |

| Total Interest Paid | $2,887 | $4,711 | +$1,824 (That’s bad!) |

| Total Cost | $33,696 | $35,520 | +$1,824 (The real cost!) |

| Loan Status after 4 Yrs | PAID OFF! | Still owe ~$9,000 | Ouch! |

The calculator instantly reveals the trap. While Chloe would “save”

167permonth,shewouldpayanextra∗∗167 per month, she would pay an extra **167permonth,shewouldpayanextra∗∗

1,824** for the exact same car. Worse, after four years, instead of owning the car free and clear, she’d still have two more years of payments. This simulation alone is worth thousands of dollars.

Strategy 2: The Power of Extra Payments

What if Chloe could find an extra $50 in her budget each month to put towards her car loan? Most advanced calculators have a feature to show the impact of extra payments.

On her original 48-month loan, if Chloe paid $627 instead of $577 each month:

- Loan Payoff: She would pay off the loan in 44 months instead of 48, saving 4 months of payments.

- Interest Saved: She would save approximately $250 in interest.

It might not seem like a fortune, but it’s her money, and she gets to own her car sooner. It demonstrates the power of paying down principal faster.

Strategy 3: Using the Calculator in the Dealership

This is the ultimate pro move. You have your pre-approval rate. You have negotiated the OTD price. The finance manager presents you with their loan terms.

Instead of just looking at their monthly payment, pull out your phone and run their numbers through your own calculator.

- Dealer Offer: “$24,809 for 60 months at 5.9%. Your payment is only $476!”

- Your Calculator: You plug in those numbers. You see the total interest paid is $3,751. You also see the total cost is now over $35,000.

- Your Response: “Thank you for the offer. I see that over five years, I’ll be paying about $900 more in interest compared to my credit union’s 48-month loan. Can you match my credit union’s 5.5% rate on a 48-month term? If so, we have a deal.”

You are now negotiating from a position of power and clarity. You’re not arguing about a monthly payment; you’re discussing the total cost of borrowing, and they know they’re dealing with an informed buyer.

Chapter 5: Blind Spots: What the Car Loan Calculator Doesn’t Tell You

The calculator is a financial tool, not a crystal ball. It’s brilliant for calculating the cost of the loan, but it knows nothing about the total cost of ownership. To be truly prepared, you must consider these critical external factors.

1. Car Insurance

The cost of insurance is a major, mandatory part of your monthly car expense. A sporty two-door coupe will have a vastly different insurance premium than a sensible four-door sedan. A 17-year-old male driver will pay far more than a 40-year-old female driver for the exact same car.

- Action Step: Before you buy, get insurance quotes for the specific models you are considering. Add this estimated monthly premium to the calculator’s loan payment to get a truer picture of your total monthly outlay.

2. Fuel

A car with 22 miles per gallon (MPG) will cost significantly more to run than one with 38 MPG. Use the EPA’s fuel economy website (fueleconomy.gov) to compare models and estimate your annual fuel costs based on your driving habits. This can easily be a difference of

50−50-50−

100 per month.

3. Maintenance and Repairs

A new car comes with a warranty, but that doesn’t cover routine maintenance like oil changes, tire rotations, and new brake pads. And once the warranty expires, you are on the hook for all repairs. Some brands are notoriously more expensive to maintain than others. Research the long-term reliability and estimated maintenance costs for the models on your list.

4. Depreciation (The Silent Killer)

Depreciation is the single largest cost of owning a new car, and the calculator doesn’t show a penny of it. The moment you drive a new car off the lot, its value can drop by 10% or more. After five years, most cars are worth only 30-50% of their original price.

- Why it Matters: While it’s not a direct cash expense, it’s a massive loss in your net worth. The $34,000 Chloe is paying for her car might only get her $15,000 if she sells it in five years. That’s a loss of nearly $19,000. This is the strongest argument for buying a gently used, 2-3 year old car, as the first owner has already absorbed the steepest part of the depreciation curve.

Conclusion: Drive with Confidence

The car-buying process is a complex journey, filled with emotional highs and financial hurdles. It’s a world where clarity can feel intentionally obscured, and a great deal can seem just out of reach.

The car loan calculator is your flashlight in the fog.

It is more than a simple math tool. It is your simulator, your strategist, and your shield. It empowers you to:

- See beyond the monthly payment and understand the true, total cost of your vehicle.

- Compare loan terms with confidence, instantly seeing the hidden price of a longer loan.

- Negotiate with facts and figures, not just feelings.

- Build a realistic budget that includes not just the loan, but all the costs of ownership.

Don’t walk onto that dealership lot unprepared. Open a car loan calculator right now. Plug in the numbers for your dream car. Test a shorter loan term. See the impact of a larger down payment. Turn anxiety into action, and confusion into confidence.

By mastering this simple tool, you ensure that when you finally get the keys and breathe in that new car smell, it’s the scent of a smart financial victory.