Demystifying Your Debt: The Power of a Loan Calculator

…

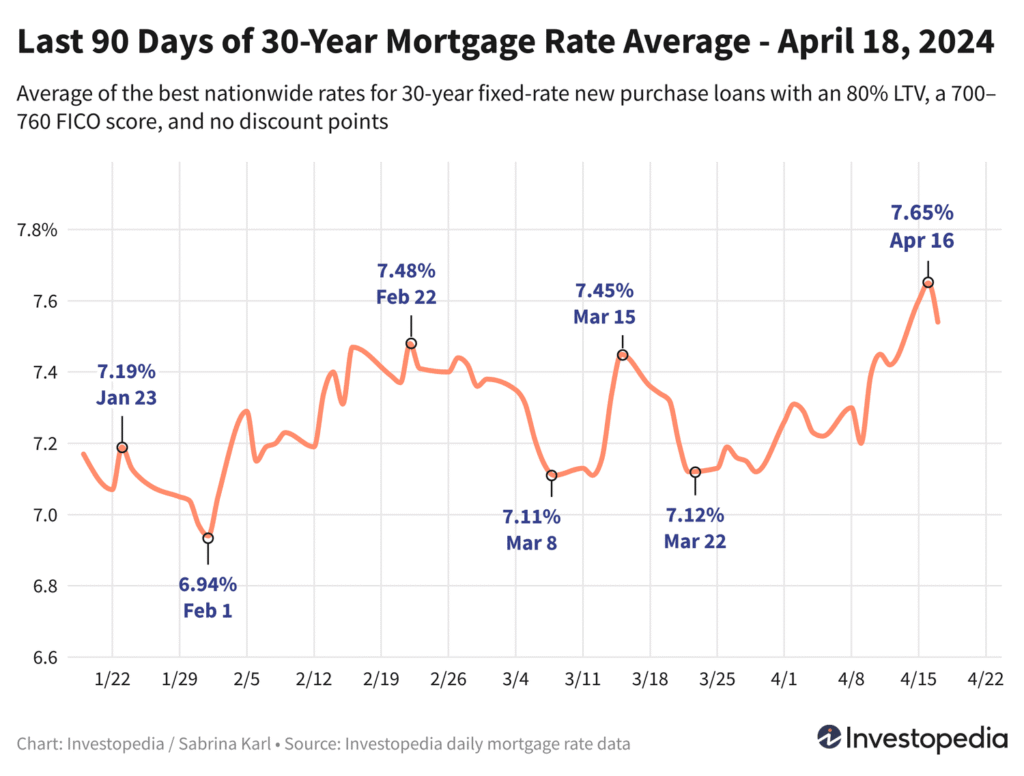

Visualizing a Loan Calculator

Here’s an example of what a typical loan calculator interface looks like and the results it might provide:

Loan Details

Or

Monthly payments

…

Understanding Loan Calculators

When it comes to borrowing money, understanding your financial obligations is crucial. Loan calculators have become indispensable tools for individuals and businesses alike to estimate payments, compare loan options, and gain clarity on financial commitments. But with so many different types of loan calculators available, how do you know which one is right for your situation? Let’s break it down.

What is a Loan Calculator?

A loan calculator is a digital tool designed to help borrowers estimate the cost of a loan. By inputting details such as loan amount, interest rate, loan term, and payment frequency, you can quickly calculate monthly payments, total interest, and the overall cost of the loan. These calculators are particularly useful for comparing loan options before committing to any financial agreement.

Types of Loan Calculators

Not all loans are created equal, and the same goes for loan calculators. Depending on your borrowing needs, you’ll want to use a specific type of loan calculator tailored to your situation. Here are some of the most common types:

1. Mortgage Loan Calculators

Mortgage calculators are designed to help potential homeowners estimate monthly payments and overall costs when buying a property. These calculators often take into account factors like property taxes, homeowner’s insurance, and private mortgage insurance (PMI). Some advanced versions even allow you to see how extra payments or refinancing options can affect your loan.

2. Auto Loan Calculators

Shopping for a car? Auto loan calculators help you determine how much car you can afford by factoring in the loan amount, interest rate, loan term, and, in some cases, sales tax and down payment. These calculators are perfect for comparing dealer financing options and bank loans.

3. Personal Loan Calculators

Personal loans are versatile financial products used for everything from consolidating debt to funding home improvements. A personal loan calculator can show you the monthly payment and total cost based on the loan terms, making it easier to decide if a personal loan is the right choice for your needs.

4. Student Loan Calculators

For students and families planning for higher education expenses, student loan calculators are essential. These tools can help estimate monthly payments based on factors like interest rates, loan forgiveness programs, and repayment plans. They’re particularly useful for understanding the long-term impact of borrowing for college.

5. Business Loan Calculators

Entrepreneurs and business owners often rely on business loans to fund operations, expansion, or equipment purchases. Business loan calculators help you analyze different financing options, taking into account loan terms, interest rates, and repayment schedules to ensure your business can meet its financial obligations.

Benefits of Using a Loan Calculator

Loan calculators offer several advantages, including:

- Clarity and Transparency: Understand the true cost of borrowing, including interest and fees.

- Better Decision-Making: Compare multiple loan options to find the best fit for your needs.

- Financial Planning: Plan your budget more effectively by knowing your monthly payment obligations in advance.

- Time Savings: Quickly calculate loan costs without needing to manually crunch numbers.

How to Choose the Right Loan Calculator

Selecting the right loan calculator depends on your specific borrowing needs. Here are a few tips:

- Identify Your Loan Type: Whether it’s a mortgage, auto loan, or personal loan, choose a calculator designed for that specific purpose.

- Look for Customization Options: Some calculators allow you to add extra details like taxes, fees, or additional payments.

- Use Trusted Sources: Financial institutions, government websites, and reputable financial tools often provide reliable calculators.

Final Thoughts

Loan calculators are powerful tools that can save you time, money, and stress when navigating the borrowing process. By using the right calculator for your loan type, you can make informed decisions and set yourself up for financial success. Whether you’re buying a home, financing a car, or funding your education, these tools provide the clarity needed to borrow responsibly.

So next time you’re considering a loan, take advantage of a loan calculator to empower your financial decisions. It’s a small step that can make a big difference in your financial journey.

FAQ: Loan Types

1. What are the main types of loans available?

The main types of loans include personal loans, auto loans, mortgage loans, student loans, business loans, and payday loans.

2. What is a personal loan?

A personal loan is an unsecured loan that can be used for various purposes, such as debt consolidation, medical bills, or home improvements. It typically has fixed interest rates and monthly payments.

3. What is a mortgage loan?

A mortgage loan is a type of loan used to purchase real estate. It is secured by the property itself, and repayment terms usually range from 15 to 30 years.

4. What is the difference between secured and unsecured loans?

Secured loans require collateral, such as a car or house, while unsecured loans are not backed by collateral and are based on the borrower’s creditworthiness.

5. What is an auto loan?

An auto loan is a secured loan used to finance the purchase of a vehicle. The car serves as collateral until the loan is fully paid off.

6. What is a student loan?

A student loan is designed to help cover the costs of education, including tuition, books, and living expenses. These loans may be offered by the government or private lenders.

7. What is a payday loan?

A payday loan is a short-term, high-interest loan intended to cover expenses until the borrower’s next paycheck. These loans typically have higher fees and shorter repayment terms.

8. What is a business loan?

A business loan is designed to help businesses cover startup costs, expansion, or operational expenses. They can be secured or unsecured, depending on the lender’s requirements.

9. How do fixed and variable interest rates differ?

Fixed interest rates remain constant throughout the loan term, while variable interest rates can fluctuate based on market conditions.

10. What factors should I consider when choosing a loan type?

Consider the loan purpose, interest rates, repayment terms, fees, and your financial situation before selecting the loan that best meets your needs.