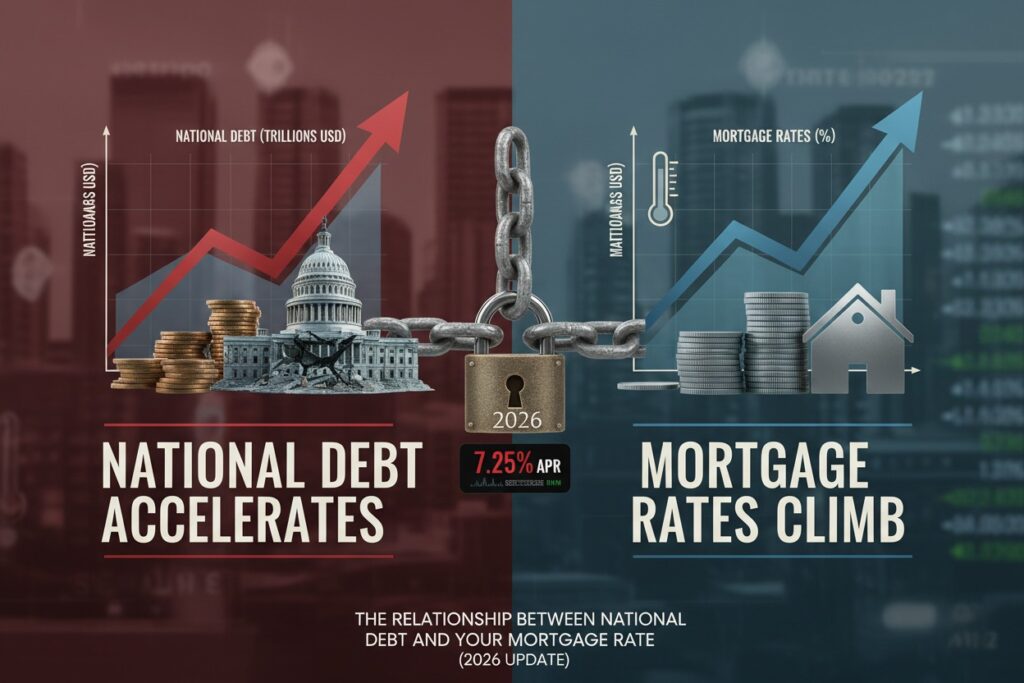

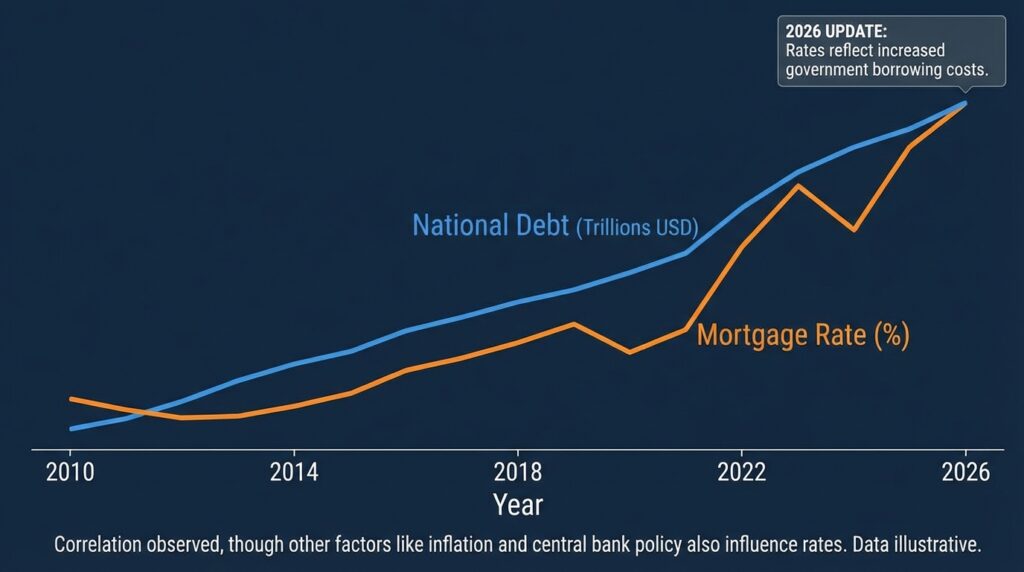

The Relationship Between National Debt and Your Mortgage Rate (2026 Update): In March 2026, the U.S. national debt has surged past $38.7 trillion. While that number feels like an abstract political problem, it has a direct, mathematical impact on the monthly payment you send to your mortgage servicer.

To understand why, you have to look past the Federal Reserve and toward the 10-year Treasury yield, which serves as the “engine room” for mortgage pricing.

1. The Anchor: The 10-Year Treasury Yield

Lenders do not set mortgage rates based on the Federal Funds Rate (the rate banks charge each other). Instead, they look at the 10-year Treasury yield.

- The Connection: Most 30-year mortgages are actually paid off or refinanced within 10 years. Therefore, investors treat mortgage-backed securities (MBS) and 10-year government bonds as similar long-term assets.

- The Spread: Lenders take the 10-year Treasury yield (currently hovering near 4.1%) and add a “spread” (usually 1.5% to 3%) to account for risk.

- The Result: This is why even when the Fed cuts short-term rates, your mortgage rate might stay at 6.0% if the 10-year yield remains elevated.

2. The “Crowding Out” Effect

When the national debt grows, the government must issue more bonds to fund its $1.9 trillion annual deficit. In 2026, this has led to a phenomenon called Crowding Out.

- High Supply: To attract enough buyers for the massive influx of new bonds, the U.S. Treasury must offer higher interest rates.

- Competition for Capital: If the government is offering 4.5% on a “risk-free” bond, mortgage lenders must offer 6% or 7% to convince investors to buy home loans instead.

- The Math: Empirical research suggests that for every 1 percentage point increase in the national debt-to-GDP ratio, interest rates rise by approximately 3 to 4 basis points ($0.03\% – 0.04\%$). With debt now at 124% of GDP, those basis points have added up to a significant permanent “surcharge” on your home loan.

3. The “Risk Premium” of 2026

In early March 2026, geopolitical tensions in the Middle East have caused a “spike” in oil prices, leading to renewed inflation fears. This creates a Risk Premium in the bond market.

- Investor Hesitation: When the national debt is high, investors worry about the government’s long-term ability to repay or its temptation to “inflate the debt away.”

- Higher Demands: To compensate for this perceived risk, investors demand even higher yields on long-term debt. This pushes the 10-year Treasury yield up, which immediately pulls mortgage rates upward.

4. 2026 Mortgage Market Snapshot

Despite the Federal Reserve making several cuts to the base rate over the last year, the sheer volume of national debt has kept mortgage rates from dropping to the “3% dreams” of the pandemic era.

| Metric | March 2026 Data | Impact on You |

| National Debt | $38.7 Trillion | High supply of bonds = Higher rates |

| 10-Year Treasury | ~4.10% | The baseline for your mortgage |

| 30-Year Fixed Rate | 6.00% | The current market reality |

| Annual Deficit | $1.9 Trillion | Sustains upward pressure on yields |

5. Summary: Why Your Rate Isn’t Lower

You might see the Federal Reserve cutting rates and wonder why your “Pre-Approval” letter still shows 6%. The national debt is the primary reason.

- More Borrowing = More Yield: The government is competing with you for the same pool of investor money.

- Inflation Expectations: High debt often signals future inflation, and lenders charge you more today to protect themselves against the shrinking value of the dollar tomorrow.

- The “Floor”: The national debt has effectively raised the “floor” for interest rates. Most experts now believe that 5.5% to 5.75% is the new “low” for the foreseeable future, rather than the 3% seen in 2021.

Conclusion: Watching the Deficit to Time Your Purchase

If you are planning to buy a home in late 2026 or 2027, don’t just watch the Federal Reserve’s headlines. Watch the U.S. Treasury’s auction results and the 10-year yield. As long as the national debt continues its rapid climb, the “downward” movement of mortgage rates will be slow, stubborn, and limited.