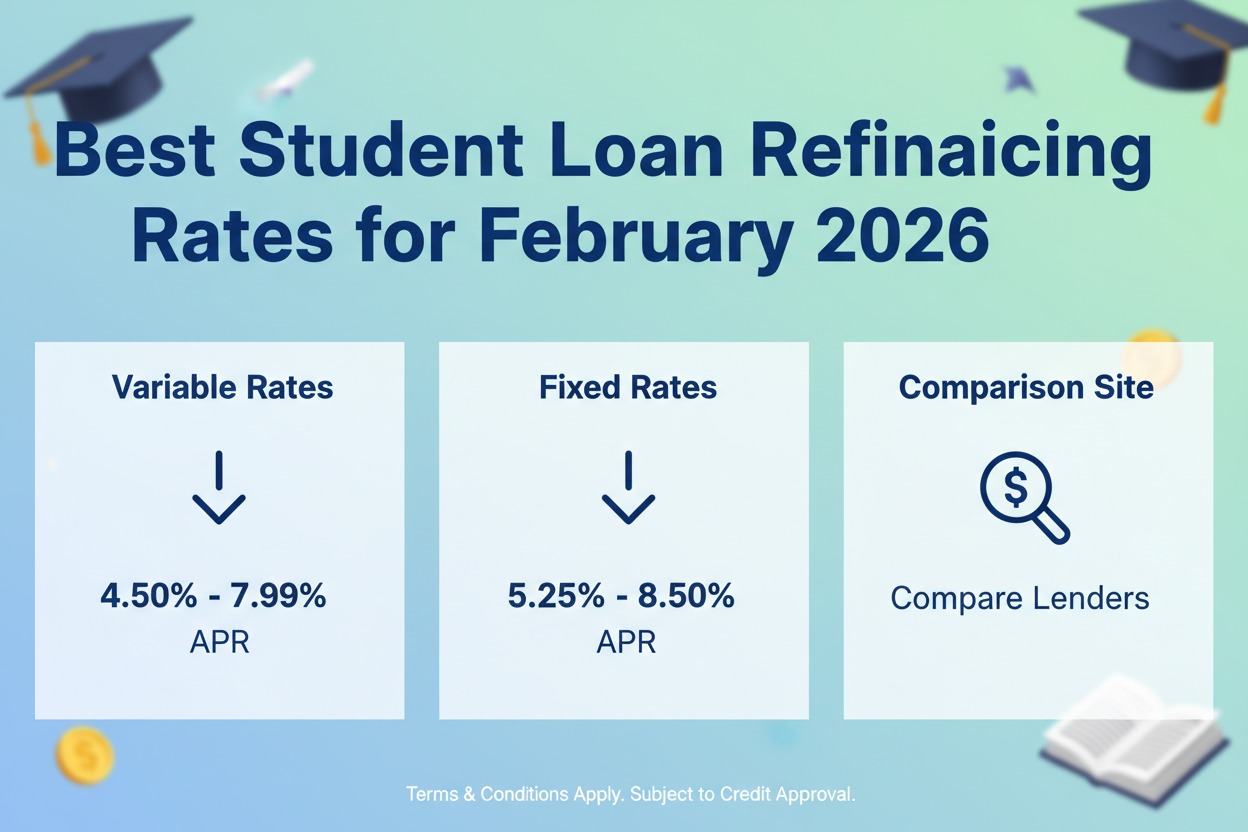

By February 2026, student loan refinancing rates have stabilized following a period of market volatility. With the 10-year Treasury yield hovering around 4.15%, top-tier lenders are offering fixed rates starting as low as 3.71% for highly qualified borrowers.

If you are looking to lower your monthly payment or escape a high-interest private loan, here is the state of the market for early 2026.

1. Top Refinance Lenders: February 2026 Comparison

The following rates reflect “as low as” pricing, which typically requires a high credit score (740+), a stable debt-to-income ratio, and enrollment in autopay.

| Lender | Fixed APR Range | Variable APR Range | Best For |

| Earnest | 3.71% – 9.99% | 5.88% – 9.99% | Customizing your monthly payment |

| RISLA | 3.99% – 8.32% | N/A (Fixed Only) | Low maximum rates |

| SoFi | 4.24% – 9.99% | 5.99% – 9.99% | Member benefits & career coaching |

| LendKey | 4.39% – 9.24% | 4.19% – 9.24% | Community banks & credit unions |

| ELFI | 4.29% – 8.44% | 4.74% – 8.24% | Large balances & medical pros |

2. Why Fixed Rates are Winning in 2026

In the current economic climate, Fixed APRs are significantly more popular than variable ones.

- Rate Parity: As of February and March 2026, many lenders have fixed rates that are actually lower than their variable starting rates.

- The Safety Play: With the 10-year Treasury yield showing minor upward ticks, locking in a rate below 4.5% is considered a strong defensive move against potential future inflation.

3. Federal vs. Private: The 2026 Dilemma

Before you refinance your federal loans in 2026, you must weigh the interest savings against the loss of government benefits.

- Federal Interest Rates (2025-2026): Undergraduate Direct loans are currently set at 6.39%, while Graduate PLUS loans are at 8.94%.

- The Refinance Benefit: If you are a graduate student with a Direct PLUS loan at 8.94%, refinancing with Earnest or RISLA at ~4.5% could save you over $200 per month on a $100,000 balance.

- The Risk: Refinancing federal loans into a private one permanently removes your access to Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) plans.

4. How to Qualify for the Lowest 2026 Rates

Lenders have tightened their standards this year. To hit the “starting” rates (under 4%), you generally need:

- A Credit Score of 750+: While 650 is the minimum for most, only the top tier gets the sub-4% rates.

- The “Autopay” Discount: Most lenders (SoFi, Earnest, ELFI) include a 0.25% discount in their advertised lowest rate, which requires you to set up automatic monthly withdrawals.

- Degree Completion: Most top-tier lenders (excepting RISLA or MEFA) require a completed Associate’s, Bachelor’s, or Graduate degree to qualify for refinancing.

5. Summary Checklist for February 2026

- [ ] Check Your DTI: Ensure your debt-to-income ratio is under 40% before applying.

- [ ] Compare the “Spread”: Look at the 10-year Treasury yield; if it spikes, refinance rates will follow within 48 hours.

- [ ] Soft Pull Only: Use lenders like SoFi or Credible that allow you to check your rate without a “hard” credit pull that could ding your score.

Conclusion: Is it the right time?

With rates for top-tier borrowers currently sitting between 3.7% and 4.5%, February 2026 is an excellent window for those stuck in private loans with double-digit interest. However, if you hold federal loans, only refinance if your job is stable and you do not plan to use government forgiveness programs.