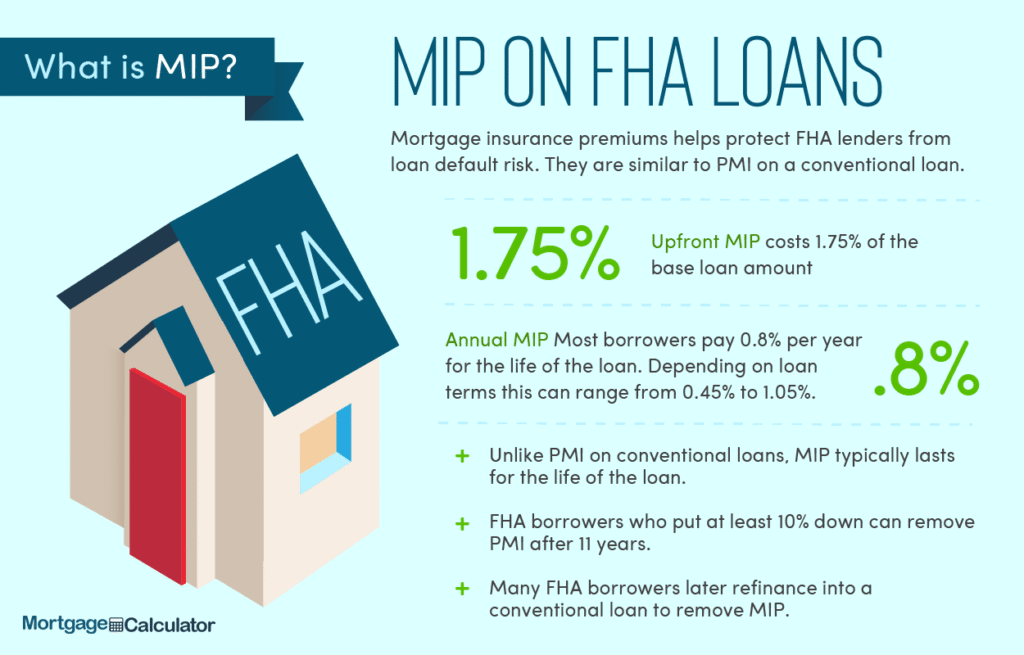

Juggling multiple credit cards can feel like a never-ending game of financial whack-a-mole. High interest rates, minimum payments, and confusing statements can quickly lead to overwhelming debt. But don’t worry, you’re not alone! Millions struggle with credit card debt, and there are proven strategies to help you consolidate your debt and regain control of your finances.

Understanding Your Debt

Before you can tackle your debt, you need to understand it. Gather all your credit card statements and list each card’s balance, interest rate, minimum payment, and due date. This will give you a clear picture of your overall debt and help you make informed decisions.

The Benefits of Consolidation

Consolidating your credit card debt offers several key advantages. A lower interest rate can significantly reduce your monthly payments and shorten the time it takes to pay off your debt. Simplifying your payments to a single monthly payment makes budgeting easier and reduces the risk of missed payments. It can also improve your credit score over time, provided you manage the consolidated debt responsibly. Learn more about credit score improvement.

Methods for Consolidation

There are several ways to consolidate your credit card debt. You can consider a balance transfer credit card, which offers a temporary 0% introductory APR. However, be aware of balance transfer fees and the interest rate after the introductory period ends. Another option is a personal loan, which often comes with a fixed interest rate and a set repayment schedule. Compare personal loan options here. Finally, you might explore a debt consolidation program, but be cautious and research thoroughly to avoid scams. [IMAGE_2_HERE]

Choosing the Right Strategy

The best strategy for you will depend on your specific financial situation and the amount of debt you owe. Factors to consider include the interest rates offered, any associated fees, and your ability to make consistent monthly payments. It’s often helpful to consult a financial advisor to guide you through this process.

Creating a Budget

Once you’ve chosen your consolidation method, creating a realistic budget is crucial. Track your income and expenses carefully, and allocate sufficient funds to your debt repayment. Consider cutting back on non-essential expenses to free up more money for debt reduction. [IMAGE_3_HERE]

Staying on Track

Paying off your consolidated debt requires discipline and consistency. Set realistic goals, and track your progress regularly. Reward yourself for milestones achieved, but avoid impulsive spending that could derail your progress. Consider using budgeting apps or spreadsheets to stay organized. Download our free budgeting template.

The Importance of Financial Literacy

Understanding your finances is key to avoiding future debt problems. Take the time to learn about budgeting, saving, and investing. There are many free resources available online and at your local library. Check out these helpful resources.

Seeking Professional Help

If you’re struggling to manage your debt on your own, don’t hesitate to seek professional help. Credit counselors can provide guidance and support, and may be able to negotiate with your creditors on your behalf. Find a certified credit counselor near you.

By taking control of your credit card debt through consolidation and careful financial planning, you can pave the way toward a brighter financial future. Remember, consistency and planning are key!

Frequently Asked Questions

What is debt consolidation? Debt consolidation is the process of combining multiple debts into a single payment. This simplifies your payments and may result in a lower interest rate.

What are the different methods of debt consolidation? Common methods include balance transfer credit cards, personal loans, and debt management programs.

How can I choose the best debt consolidation method for me? Consider factors like interest rates, fees, and your ability to make consistent payments. Consult a financial advisor for personalized guidance.

What if I can’t afford my consolidated debt payments? Contact your lender immediately to discuss options, such as forbearance or a repayment plan. Consider seeking help from a credit counselor.

Will debt consolidation affect my credit score? While it might initially have a small negative impact, responsible management of your consolidated debt can improve your credit score over time.