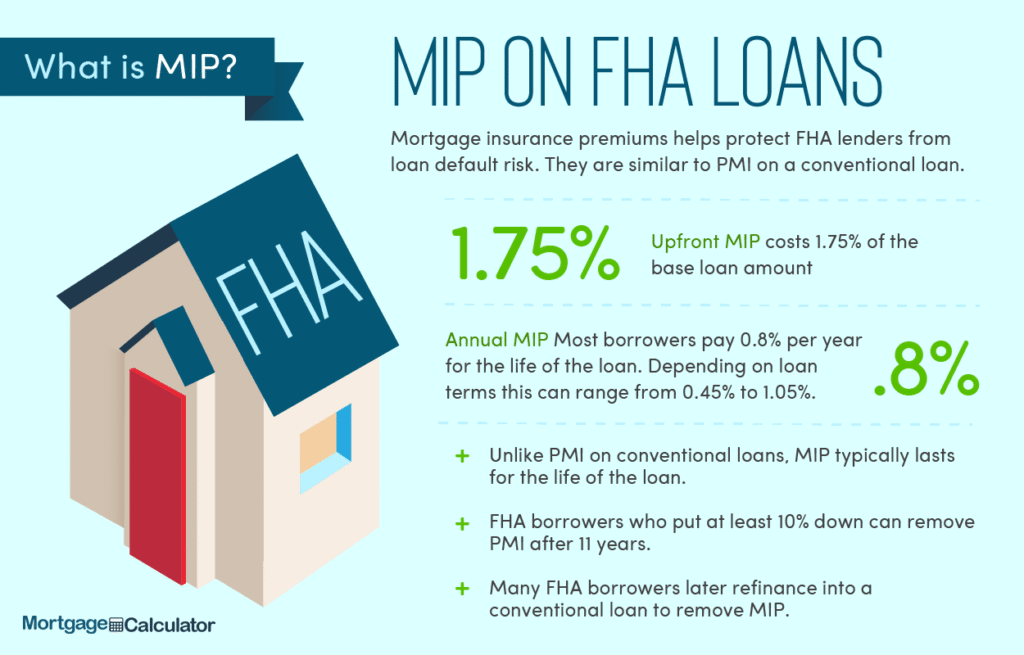

Introduction

Consolidation loans offer a way to simplify your finances by combining multiple debts into a single, manageable monthly payment. This can lead to lower monthly payments, a simpler repayment process, and potentially better interest rates. But is a consolidation loan right for you? Let’s explore.

Understanding Consolidation Loans

A consolidation loan is a new loan that pays off your existing debts, such as credit cards, personal loans, or student loans. Once consolidated, you make only one payment to your lender each month.

Types of Consolidation Loans

Several types of consolidation loans exist, each designed to address different debt situations. Common options include personal loans, debt management plans, and balance transfer credit cards. Choosing the right type depends on your specific circumstances and financial goals. Learn more about different loan types.

Benefits of Consolidating Your Debt

The benefits of consolidation can be significant. A lower monthly payment can free up cash flow, making it easier to manage your budget. Simplified repayment makes tracking your debts easier, reducing stress and the risk of missed payments. Check out this resource for more benefits.

Potential Drawbacks

While consolidation offers numerous advantages, it’s crucial to consider potential drawbacks. A longer repayment period could mean paying more interest overall. Also, consolidating high-interest debts into a lower-interest loan may not always result in significant savings. Read more about the potential downsides.

How to Qualify for a Consolidation Loan

Lenders assess your creditworthiness, income, and debt-to-income ratio when considering your application. A good credit score and a stable income are essential for approval. Improving your credit score before applying can significantly increase your chances of getting a favorable interest rate. [IMAGE_2_HERE]

Finding the Right Lender

Shopping around and comparing offers from different lenders is crucial. Consider factors like interest rates, fees, and repayment terms. Online comparison tools can help you find the best deals available in the market. Compare lenders here.

Managing Your Consolidated Debt

Once you’ve secured a consolidation loan, develop a solid repayment strategy. Creating a budget and sticking to it helps ensure timely payments. Automating your payments can also prevent missed payments and late fees. [IMAGE_3_HERE]

Conclusion

Consolidation loans can be a powerful tool for managing debt, but careful consideration is key. Weigh the pros and cons, explore your options, and choose the solution that best suits your financial situation. Remember to always seek professional financial advice when making major financial decisions. Get expert advice.

Frequently Asked Questions

What types of debt can be consolidated? Many types of debt can be consolidated, including credit card debt, personal loans, and student loans. However, some types of debt, such as medical debt, may be harder to consolidate.

How does a consolidation loan affect my credit score? Consolidating your debt can positively or negatively affect your credit score, depending on your situation and how you manage the loan. Paying off your debts on time can improve your credit score.

What are the fees associated with consolidation loans? Consolidation loans often come with fees, such as origination fees or prepayment penalties. Make sure to compare these fees across different lenders before choosing a loan. Learn more about fees and charges.

Can I consolidate debt with bad credit? It may be more challenging to qualify for a consolidation loan with bad credit, but some lenders specialize in working with borrowers who have less-than-perfect credit history. You might consider debt management programs.