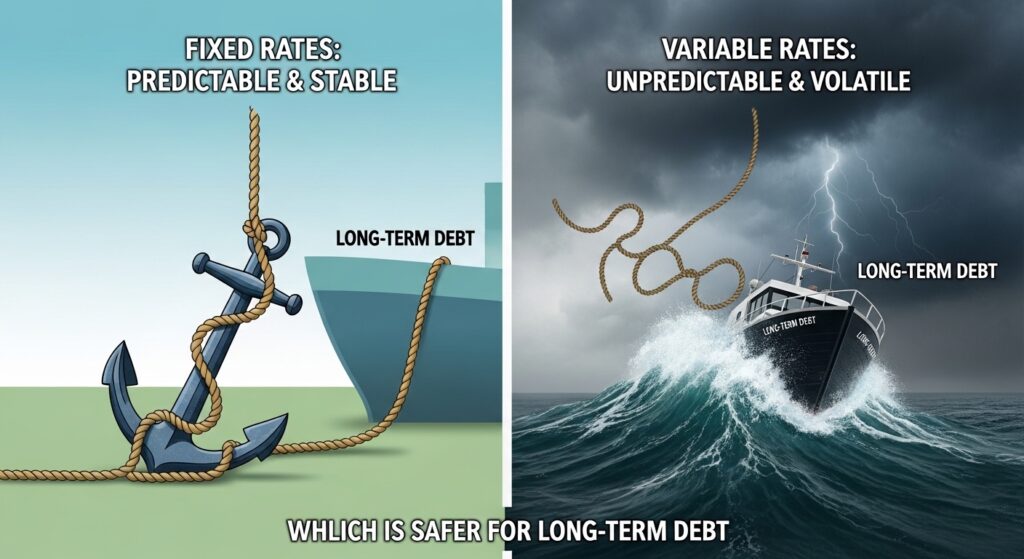

When taking on long-term debt—whether a mortgage, auto loan, or personal loan—one of the most critical decisions you’ll make is choosing between a fixed interest rate and a variable interest rate. This choice can significantly impact your financial situation over the life of the loan, affecting your monthly payments, total interest paid, and overall financial stability. Understanding the differences, advantages, and disadvantages of each option is essential for making an informed decision. This comprehensive guide explores fixed and variable rates, analyzing which is safer for long-term debt in today’s economic environment.

Understanding Fixed and Variable Rates

Fixed Interest Rates:

A fixed interest rate remains constant throughout the entire loan term. Your monthly payment stays the same from the first payment to the last, regardless of market conditions or economic changes. This predictability makes fixed-rate loans easier to budget for and provides protection against rising interest rates.

Variable Interest Rates:

A variable interest rate (also called adjustable or floating rates) changes periodically based on market conditions and a specific index. Your monthly payment may increase or decrease depending on how the underlying index moves. Variable rates typically start lower than fixed rates but can increase significantly over time.

How Variable Rates Work: The Mechanics

To understand variable rates, it’s important to understand the components that determine your rate.

Index:

The index is the benchmark rate that your variable rate is tied to. Common indices include:

- Prime Rate: The rate banks charge their most creditworthy customers

- LIBOR (London Interbank Offered Rate): A benchmark rate for short-term lending between banks

- Treasury Rates: Rates on U.S. Treasury securities

- Federal Funds Rate: The rate banks charge each other for overnight lending

Margin:

The margin is the percentage points the lender adds to the index. For example, if the prime rate is 8% and your margin is 2%, your interest rate would be 10%. The margin typically remains constant throughout the loan term.

Adjustment Period:

The adjustment period determines how often your rate can change. Common adjustment periods include:

- Annual: Rate adjusts once per year

- Semi-Annual: Rate adjusts twice per year

- Monthly: Rate adjusts once per month

Caps:

Most variable-rate loans include caps that limit how much your rate can increase:

- Periodic Cap: Limits the increase at each adjustment period (typically 1-2%)

- Lifetime Cap: Limits the total increase over the life of the loan (typically 5-6%)

- Floor: Establishes a minimum rate below which the rate cannot fall

Fixed Rates: Advantages and Disadvantages

Advantages of Fixed Rates:

Predictability: Your monthly payment never changes, making budgeting straightforward and reliable. This is particularly valuable for long-term financial planning.

Protection Against Rate Increases: If interest rates rise significantly, your rate remains unchanged. This protection can save thousands of dollars over the life of a loan.

Peace of Mind: Knowing your payment will never increase provides psychological comfort and reduces financial stress.

Easier Comparison: Fixed rates are straightforward to compare between lenders, making it easier to find the best deal.

Better for Rising Rate Environments: In periods of rising interest rates, fixed rates protect you from increasing payments.

Disadvantages of Fixed Rates:

Higher Initial Rates: Fixed rates are typically higher than the initial variable rate, sometimes 0.5-1.5% higher. This means higher initial payments and more interest paid if rates don’t rise.

No Benefit from Falling Rates: If interest rates decline, your rate remains unchanged. You won’t benefit from lower rates unless you refinance (which involves fees and a new application).

Refinancing Costs: To take advantage of lower rates, you must refinance, which involves closing costs, appraisals, and a new application process.

Opportunity Cost: In a declining rate environment, you may pay more interest than necessary with a fixed rate.

Variable Rates: Advantages and Disadvantages

Advantages of Variable Rates:

Lower Initial Rates: Variable rates typically start 0.5-1.5% lower than fixed rates. This results in lower initial payments and less interest paid in the early years of the loan.

Potential Savings in Declining Rates: If interest rates fall, your rate decreases, resulting in lower payments and less total interest paid.

No Refinancing Needed: As rates adjust, you automatically benefit from lower rates without refinancing costs.

Flexibility: Variable rates can be attractive for borrowers planning to sell or refinance within a few years.

Disadvantages of Variable Rates:

Payment Uncertainty: Your monthly payment can increase significantly, making long-term budgeting difficult and creating financial stress.

Risk of Rate Increases: In a rising rate environment, your payments can increase substantially, potentially straining your budget.

Worst-Case Scenario: With lifetime caps, your rate could increase 5-6% or more over the loan term, potentially doubling your monthly payment.

Complexity: Variable rates are more complex to understand and compare, making it harder to evaluate the true cost of the loan.

Refinancing Risk: If rates rise significantly, refinancing to a fixed rate may be expensive or impossible if your credit has declined.

Payment Shock: When rates adjust upward, the increase in monthly payments can be sudden and substantial, creating budgeting challenges.

Comparing Costs: Fixed vs. Variable Rates

To understand the financial impact of choosing fixed vs. variable rates, consider a $300,000 mortgage with a 30-year term.

Scenario 1: Stable Rate Environment

- Fixed Rate: 7.0% APR

- Initial Variable Rate: 6.0% APR

- Adjustment Period: Annual

- Lifetime Cap: 6.0%

Year 1-5 (Rates Remain Stable):

- Fixed Rate Payment: $1,996/month

- Variable Rate Payment: $1,799/month

- Savings with Variable: $197/month or $11,820 over 5 years

Year 6-30 (Rates Rise 1% Annually):

- Fixed Rate Payment: $1,996/month (unchanged)

- Variable Rate Payment: Increases from $1,799 to $2,500/month by year 12

- Total Interest Paid (Fixed): $418,512

- Total Interest Paid (Variable): $425,000

- Additional Cost with Variable: $6,488

Scenario 2: Rising Rate Environment

In a scenario where rates rise 3% over the first 5 years:

- Fixed Rate Payment: $1,996/month (unchanged)

- Variable Rate Payment: Increases from $1,799 to $2,400/month by year 5

- Savings in Years 1-5: $11,820

- Additional Payments in Years 6-30: $15,000+

- Net Result: Variable rate costs $3,000+ more over life of loan

Scenario 3: Declining Rate Environment

In a scenario where rates fall 2% over the first 5 years:

- Fixed Rate Payment: $1,996/month (unchanged)

- Variable Rate Payment: Decreases from $1,799 to $1,400/month by year 5

- Savings in Years 1-5: $11,820

- Continued Savings in Years 6-30: $8,000+

- Total Savings with Variable: $19,820

Current Economic Environment: 2026 Rate Outlook

As of February 2026, the economic environment presents unique considerations for fixed vs. variable rate decisions.

Current Rate Environment:

- 30-Year Fixed Mortgage: 7.0-7.5%

- 5/1 ARM (Adjustable Rate Mortgage): 6.0-6.5%

- Prime Rate: 8.25%

- Federal Funds Rate: 4.25-4.50%

Economic Factors:

The Federal Reserve has signaled that interest rates may remain elevated for the foreseeable future, with potential for further increases if inflation remains sticky. However, some economists expect rates to decline in the second half of 2026 if inflation continues to moderate.

Implications:

In this environment, fixed rates provide protection against further increases, while variable rates offer lower initial payments with the risk of increases if the Fed maintains higher rates longer than expected.

Choosing Between Fixed and Variable Rates

Choose Fixed Rates If:

- You plan to keep the loan for the entire term

- You have a tight budget and need payment predictability

- You believe interest rates will rise

- You prefer peace of mind over potential savings

- You have variable income and need stable payments

- You’re in a rising rate environment

Choose Variable Rates If:

- You plan to sell or refinance within 5-7 years

- You have a flexible budget and can handle payment increases

- You believe interest rates will fall

- You’re comfortable with risk for potential savings

- You have stable, predictable income

- You’re in a declining rate environment

Hybrid Approach:

Some borrowers use a hybrid approach, such as a 5/1 ARM (fixed for 5 years, then adjustable). This provides:

- Lower initial rates than a 30-year fixed

- Protection for the first 5 years

- Flexibility if you plan to sell or refinance within 5 years

- Reduced risk compared to a fully variable rate

Strategies for Managing Variable Rate Risk

If you choose a variable rate, several strategies can help manage the risk of rate increases.

Rate Caps:

Ensure your loan has reasonable rate caps. A periodic cap of 1-2% and a lifetime cap of 5-6% limits your maximum exposure.

Refinancing Option:

Maintain the ability to refinance to a fixed rate if rates rise significantly. Keep your credit score strong and avoid taking on additional debt.

Payment Planning:

Budget for potential rate increases. If your initial payment is $1,500, budget for a potential increase to $1,800-$2,000 to prepare for rate adjustments.

Early Payoff:

Consider paying extra toward principal in the early years when rates are low. This reduces the balance subject to future rate increases.

Rate Monitoring:

Monitor interest rate trends and be prepared to refinance to a fixed rate if rates rise significantly and refinancing becomes attractive.

Long-Term Debt Considerations

For truly long-term debt (15+ years), fixed rates generally offer more safety and predictability. Here’s why:

Uncertainty Over Long Periods:

The longer the loan term, the more uncertain future rate movements become. Fixed rates eliminate this uncertainty.

Compounding Effects:

Over 30 years, even small rate increases compound significantly. A 2% increase over 30 years can add $100,000+ to the total cost of a mortgage.

Life Changes:

Over 15-30 years, your financial situation may change dramatically. Fixed rates provide stability regardless of life changes.

Inflation Protection:

Fixed-rate debt becomes easier to pay off as inflation increases your income over time. With a fixed payment, inflation effectively reduces the real cost of the debt.

Recent Trends and Historical Context

Historical Rate Comparisons:

- 1980s: Fixed mortgage rates reached 18%+

- 2000s: Fixed rates averaged 6-7%

- 2010s: Fixed rates declined to 3-4%

- 2020-2021: Fixed rates hit historic lows of 2.7-3.0%

- 2022-2026: Fixed rates increased to 6.5-8.0%

Variable Rate Trends:

Variable rates have historically been 1-2% lower than fixed rates initially, but can increase 5-6% or more over the loan term in rising rate environments.

Conclusion: Which is Safer for Long-Term Debt?

For most borrowers with long-term debt obligations, fixed rates are generally safer. Here’s why:

- Predictability: Fixed rates provide payment certainty, making long-term budgeting possible

- Protection: Fixed rates protect against rising rates, which is the most likely scenario over 15-30 years

- Peace of Mind: Knowing your payment won’t increase reduces financial stress

- Inflation Benefit: Fixed payments become easier to manage as inflation increases your income

- Simplicity: Fixed rates are easier to understand and compare

However, variable rates can be appropriate for borrowers who:

- Plan to sell or refinance within 5-7 years

- Have flexible budgets and can handle payment increases

- Believe rates will fall

- Are comfortable with risk for potential savings

The key is understanding your financial situation, risk tolerance, and long-term plans. For most borrowers seeking true long-term debt safety, fixed rates provide the stability and predictability necessary for successful financial planning.

Quick Reference: Fixed vs. Variable Comparison

| Factor | Fixed Rate | Variable Rate |

|---|---|---|

| Initial Payment | Higher | Lower |

| Payment Predictability | Guaranteed | Uncertain |

| Rate Risk | Protected | Exposed |

| Refinancing | Required for lower rates | Automatic adjustments |

| Best For | Long-term debt | Short-term debt |

| Budget Impact | Stable | Potentially volatile |

| Total Interest (Rising Rates) | Lower | Higher |

| Total Interest (Falling Rates) | Higher | Lower |

| Complexity | Simple | Complex |

| Peace of Mind | High | Lower |