In 2026, the Federal Reserve’s decisions remain the “engine” behind auto loan pricing. While the Fed doesn’t set car loan rates directly, their benchmark federal funds rate acts as the foundation upon which lenders build your interest offer.

1. The “Domino Effect” in 2026

When the Federal Reserve raises rates (as seen in the early 2020s), the cost for banks to borrow money increases. To maintain their profit margins, they pass these costs to you.+1

- Fed Funds Rate ⮕ Prime Rate ⮕ Your APR: Lenders typically use the Prime Rate (which is usually 3% above the Fed’s rate) as a baseline for auto loans.

- Lag Time: Auto loans are “sticky.” While credit card rates jump almost instantly after a Fed hike, car loan rates often take 2 to 4 weeks to adjust at the dealership level.

2. Impact Analysis: The “1% Rule”

For most car buyers, a 1% increase in your interest rate may sound small, but it adds up significantly over the life of a 60-month or 72-month loan.

The Math: $35,000 New Car Loan (60 Months)

| Scenario | Interest Rate (APR) | Monthly Payment | Total Interest Paid |

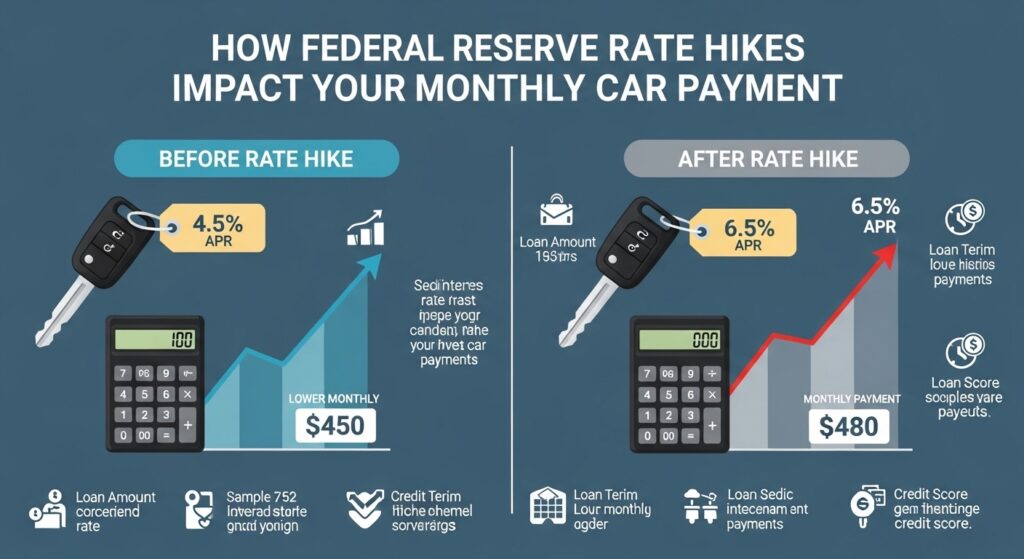

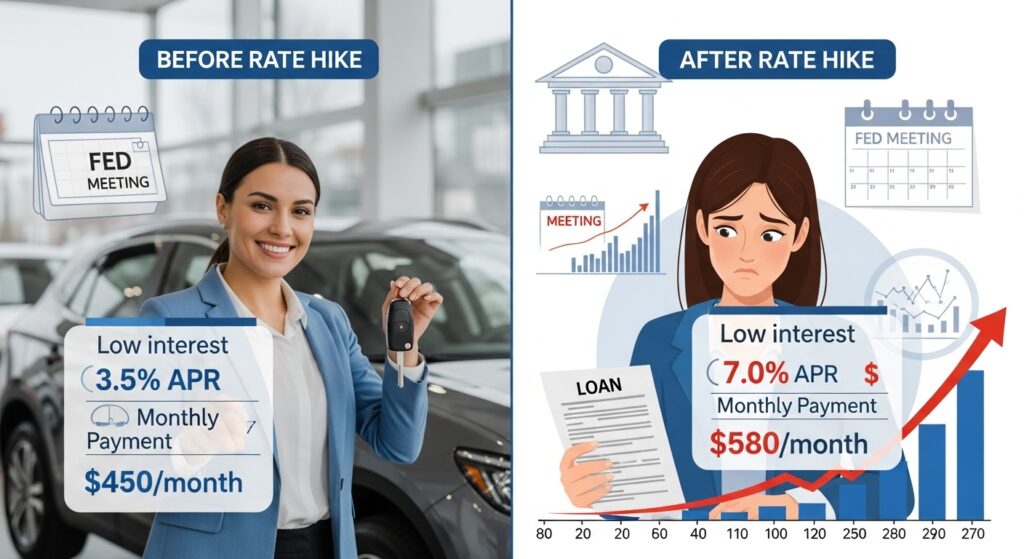

| Fed Rate Cut (2025/26 Low) | 5.5% | $668 | $5,080 |

| Fed Rate Hike (+1%) | 6.5% | $685 | $6,100 |

| Fed Rate Hike (+2%) | 7.5% | $701 | $7,060 |

The 2026 Takeaway: A simple 1% hike adds roughly $17/month to your bill and over $1,000 in total interest. That’s essentially the cost of a high-end sound system or a premium leather upgrade—lost to interest.

3. Why Used Cars Feel the “Heat” More

If you are buying used in 2026, Fed hikes hit harder. Used car loans are perceived as riskier by banks, so they often carry a 3% to 5% premium over new car rates.

- New Car Average (2026): ~7.01%

- Used Car Average (2026): ~11.5% – 14.1%

When the Fed hikes by 0.25%, used car lenders often use it as a reason to hike their specific rates by 0.50% or more, especially for “Fair” credit (650 range) buyers.

4. Fixed vs. Variable: Why You Might Be Safe

- Most Auto Loans are Fixed: If you signed your paperwork in 2024 or 2025, your monthly payment is locked. Federal Reserve hikes in 2026 will not increase your current payment.

- The Refinance Risk: The real impact is on those waiting to refinance. If you were hoping to swap a high-interest loan for a lower one, a Fed hike “closes the window” on your potential savings.

5. Your 2026 “Fire Horse” Maneuvers

Because 2026 is a year of momentum and sudden pivots, use these three tactics to beat the Fed:

- Lock Your Rate Early: Most Credit Unions (like PenFed or Navy Federal) offer “Rate Locks” for 30–60 days. If a Fed meeting is coming up and a hike is rumored, get your pre-approval locked now.

- Shorten the Fuse: A 48-month loan almost always carries a lower APR than a 72-month loan because the bank has less time to be exposed to Fed rate volatility.

- The “Incentive” Hunt: In 2026, manufacturers (like Ford, Toyota, and Tesla) are offering subsidized financing (e.g., 1.9% or 2.9% APR) to move inventory. These rates are “divorced” from the Fed because the manufacturer is paying the difference to get you in the car.

Summary Checklist

- Hike = Higher monthly payment + Higher total cost.

- Credit Score = Your best defense. A 100-point score increase saves you more than a 1% Fed rate cut.

- Target = Aim for Credit Unions in 2026; they often delay passing on Fed hikes longer than big banks.