Create a 50/30/20 budget is one of the most effective ways to manage your money in 2026. This simple framework, popularized by Senator Elizabeth Warren, helps you move away from tracking every penny and toward a high-level strategy that ensures your future is funded while you still enjoy your present.

1. The 50/30/20 Rule Broken Down

The rule is based on your after-tax income (the amount that actually hits your bank account). You divide that total into three “buckets”:

🏠 50% for “Needs”

These are the non-negotiables. If you stopped paying these, your life would be significantly disrupted.

- Housing: Rent or mortgage and property taxes. Create a 50/30/20 budget

- Utilities: Electricity, water, gas, and basic internet/phone.

- Groceries: Essential food and household supplies (not luxury dining).

- Transportation: Car payments, gas, insurance, or public transit passes.

- Minimum Debt: The absolute minimum payments required on all loans.

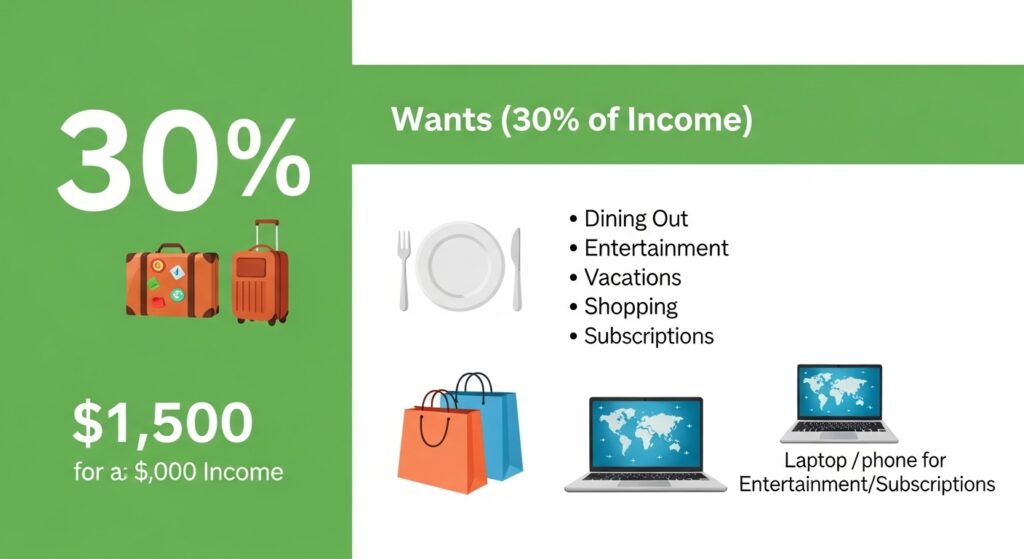

🍕 30% for “Wants”

This is your “lifestyle” category. These are the things that make life fun but aren’t strictly necessary for survival.

- Dining Out: Coffee shops, bars, and restaurants. Create a 50/30/20 budget

- Entertainment: Movies, concerts, and streaming services (Netflix, Spotify).

- Hobbies: Gym memberships, sports, and creative projects.

- Travel: Vacations and weekend getaways.

💰 20% for “Savings & Debt Repayment”

This is the most important bucket for your future self.

- Emergency Fund: Building a 3–6 month cushion.

- Retirement: Contributions to your 401(k) or IRA.

- Aggressive Debt Payoff: Any payments made above the minimum to kill high-interest debt (like credit cards).

- Investments: Stocks, bonds, or real estate funds.

2. How to Calculate Your 2026 Numbers

To get your specific dollar amounts, follow this simple math:

- Calculate Take-Home Pay: Look at your monthly bank deposits. If your employer deducts for health insurance or a 401(k), add those back in to get a true “net income” starting point. Create a 50/30/20 budget

- Multiply by 0.50: This is your maximum budget for Needs.

- Multiply by 0.30: This is your maximum budget for Wants.

- Multiply by 0.20: This is your minimum target for Savings.

Example: If your monthly take-home pay is $4,000:

- Needs: $2,000

- Wants: $1,200

- Savings: $800

3. Your Free 2026 Budget Template

You don’t need expensive software. You can copy this structure into a simple Excel or Google Sheets file:

| Category | Item | Budgeted ($) | Actual ($) | Difference |

| NEEDS (50%) | Rent/Mortgage | |||

| Utilities | ||||

| Groceries | ||||

| Total Needs | $0.00 | $0.00 | $0.00 | |

| WANTS (30%) | Dining Out | |||

| Subscriptions | ||||

| Hobbies | ||||

| Total Wants | $0.00 | $0.00 | $0.00 | |

| SAVINGS (20%) | Emergency Fund | |||

| Retirement | ||||

| Debt Payoff | ||||

| Total Savings | $0.00 | $0.00 | $0.00 |

4. Why 2026 is Different: The “Adjustment” Strategy

In 2026, the cost of “Needs” (especially housing and insurance) has stayed high. If your Needs exceed 50%, do not panic.

- The 60/20/20 Variation: If you live in a high-cost city, your Needs may realistically hit 60%. In this case, pull 10% from your “Wants” category, keeping your “Savings” at a strict 20%.

- The Debt-First Approach: If you have high-interest credit card debt (above 15%), treat your 20% “Savings” bucket as a “Debt Destroyer” bucket until the cards are at zero.

Conclusion

The 50/30/20 rule is a marathon, not a sprint. The goal isn’t to be perfect in month one; it’s to gain awareness of your spending habits. Once you see that your “Wants” are taking up 45% of your income, you finally have the data you need to make a change.