How to Get a Low-Interest Personal Loan with a 650 Credit Score: A 650 credit score is categorized as “Fair” in the 2026 economic landscape. While you are above the “Bad” credit threshold, you are currently in a “swing” zone where your strategy can mean the difference between a 12% APR and a 29% APR.

Here is how to navigate the 2026 lending market to secure the lowest possible rate on YourFinanceRates.com.

🏗️ The 2026 Lending Landscape

As of February 2026, the Federal Reserve has implemented several rate cuts, bringing the average personal loan rate for “Fair” credit down to approximately 17.9% – 19.9%. However, specialized lenders and specific strategies can help you beat this average.

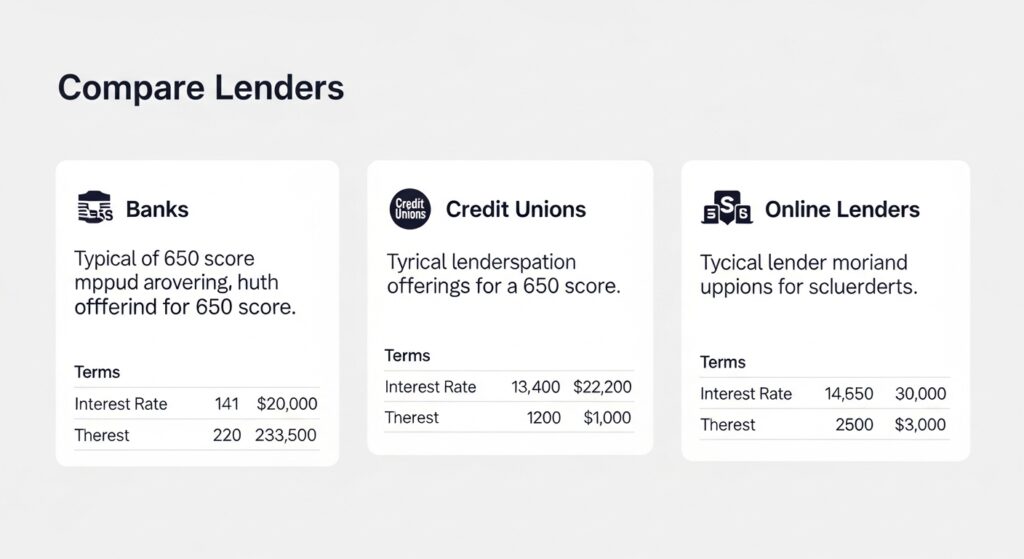

Best Lenders for a 650 Score

| Lender | Est. APR for 650 Score | Why They Fit |

| Upgrade | 14.5% – 22.0% | Known for “Fair” credit flexibility and fast funding. |

| Best Egg | 15.0% – 24.0% | Excellent for debt consolidation; offers “secured” options. |

| Upstart | 12.0% – 29.0% | Uses AI to look at your education and job history, not just your score. |

| PenFed CU | 7.9% – 17.9% | Credit Unions legally cap rates at 18%, making them a “Fair” credit sanctuary. |

🐎 5 Strategies to Lower Your Rate Today

1. The “Secured” Pivot (High Impact)

In 2026, Best Egg and Upgrade have popularized “Secured Personal Loans.” By backing your loan with a vehicle title or even home fixtures (like kitchen cabinets), you reduce the lender’s risk.+1

- The Result: This can drop your APR by 3% to 5% compared to an unsecured loan with the same 650 score.

2. Join a Credit Union (The “18% Ceiling”)

Federal credit unions have a legal interest rate cap (usually 18%). While an online lender might charge a 650-score borrower 25%, a credit union like Navy Federal or PenFed may stay closer to 12% – 15%.

- Action: Open a savings account with $5 at a local credit union 48 hours before applying for the loan to establish “membership.”

3. Add a “Credit Anchor” (Co-Signer)

The “Fire Horse” year is about partnership. If you have a family member with a 720+ score, adding them as a co-signer can anchor your rate to their credit profile.

- The Result: You could potentially qualify for “Excellent” tier rates (under 10%) even with your 650 score.

4. Opt for a Shorter Term

Lenders in 2026 are wary of long-term economic shifts. You will almost always get a lower rate on a 24-month or 36-month loan than on a 60-month loan.

- The Habit: Choose the shortest term you can realistically afford. While the monthly payment is higher, the “Cost of Capital” (interest) is significantly lower.

5. Leverage “Relationship Discounts”

If you already have a checking account with Wells Fargo or U.S. Bank, check for “Relationship Rewards.” Most major banks offer a 0.25% to 0.50% APR discount for existing customers who set up autopay from their internal accounts.

🛠️ The “Pre-Application” Checklist

Before you hit “Apply,” perform these three Financial Gymnastics moves to protect your score:

- Use Soft-Pull Marketplaces: Use sites like Credible or LendingTree to see offers. These use a “soft credit pull” that does not hurt your 650 score.

- Check for “Ghost” Debt: Ensure your credit utilization is under 30%. If you can pay down a small credit card balance to get your score to 660 (the “Good” threshold), your interest offers could drop by 2% overnight.

- Watch for Origination Fees: A “low interest” loan with a 6% origination fee is often more expensive than a “higher interest” loan with no fees. Always compare the APR, not just the interest rate.

🏮 2026 Pro Tip: The “Rate Refinance”

If you must take a loan at 19% today, don’t panic. The 2026 forecast suggests more Fed rate cuts in Q3 and Q4. Set a calendar reminder to refinance your loan in 6 months. If your score has improved to 680 by then, you could swap that 19% loan for an 11% one.

Would you like me to create a “Loan Comparison Table” showing the total cost of a $10,000 loan at 12% vs. 22% over three years?