In the 2026 financial landscape, the difference between a “good” loan and a “debt trap” often comes down to a few percentage points and a bit of math. As of March 2026, the average personal loan interest rate sits at 12.26%, while mortgage rates have finally dipped below the 6% mark.

Understanding how to use interest rate calculators isn’t just about finding your monthly payment; it’s about pulling back the curtain on the true cost of borrowing. Here is your comprehensive guide to using these tools like a financial pro.

1. The Anatomy of a Loan Calculator: What Inputs Matter?

When you open an interest rate calculator in 2026, you’ll face several fields. Accuracy here is the difference between a helpful estimate and a costly surprise.

- Principal (Loan Amount): The total amount you are borrowing.

- Interest Rate: The annual percentage charged by the lender. (Note: In 2026, “Stellar” credit might get you 6.2%, while “Average” credit is closer to 12.5%).

- Loan Term: How long you have to pay it back (e.g., 36 months for a personal loan or 30 years for a mortgage).

- Compounding Frequency: How often interest is calculated. Most personal loans and mortgages in the US compound monthly.

2. APR vs. Interest Rate: The Calculator Secret

This is the most common mistake borrowers make.

- Interest Rate is the bare cost of the money.

- APR (Annual Percentage Rate) includes the interest rate plus any lender fees (origination fees, processing fees).

The Strategy: Always plug the APR into your calculator to find your real monthly cost. If a lender offers a 10% interest rate but a 5% origination fee, your actual cost is significantly higher than a “clean” 11% loan with no fees.

3. How to Read an Amortization Schedule

Most advanced calculators provide an Amortization Schedule. This is a table showing every payment over the life of the loan.

The “Front-Loading” Reality

In the early years of a loan (especially a mortgage), your payments go almost entirely toward interest, not the principal.

- Year 1: You might pay $2,000 a month, but only $300 of that actually reduces your debt.

- Year 25: That same $2,000 payment might see $1,700 going toward the principal.

Why this matters in 2026: If you plan to sell your home or refinance your loan in 3 years, an amortization schedule will show you exactly how much debt you will still have at that time. You might be surprised at how little progress you’ve made.

4. Using the “Extra Payment” Feature to Save Thousands

One of the most powerful ways to use a calculator in 2026 is the Extra Monthly Payment field. Because interest is calculated on your remaining balance, paying even a little extra early on has a massive “snowball” effect.

Example: A $30,000 Personal Loan at 12% for 5 Years

- Standard Payment: $667/mo

- Total Interest Paid: $10,040

- With $100 Extra/mo: You pay the loan off 11 months early and save $1,980 in interest.

[Image: A comparison chart showing “Total Interest Paid” with and without extra payments]

5. Predicting Costs in a Volatile 2026 Market

In March 2026, the Federal Reserve has begun a series of “mini-cuts” to the benchmark rate. This creates a unique opportunity for Variable Rate Loans.

- Fixed Rate: Predictable. Use the calculator once, and the number stays the same.

- Variable/Adjustable Rate: Use the calculator to run a “Stress Test.” * Step 1: Run the numbers at the current rate (e.g., 6%).

- Step 2: Run them at a “Worst Case” rate (e.g., 9%).

- The Verdict: If you cannot afford the “Worst Case” payment, you should not take the variable-rate loan, regardless of how low the “teaser” rate is today.

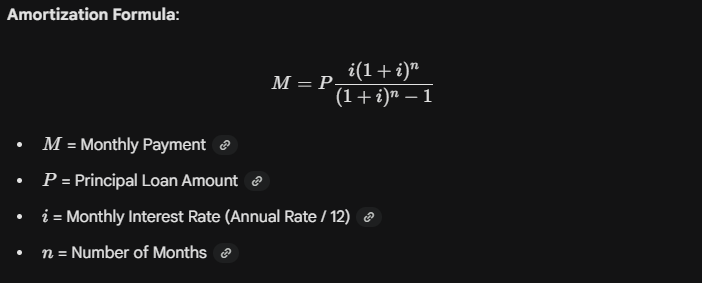

6. The Mathematical Formula (For the Curious)

If you want to understand what the calculator is doing behind the scenes, it uses the Standard Amortization Formula:

Conclusion: Tools Over Instincts

In 2026, lenders use high-level AI to determine how much they can charge you. Your best defense is a simple interest rate calculator. By running your own numbers, you can spot predatory fees, understand the “interest-heavy” early years of your loan, and find the exact “extra payment” amount that fits your budget.