Savings vs. CDs in 2026: In the ever-evolving landscape of personal finance, deciding where to park your cash remains a critical choice for many individuals. As we navigate through 2026, the decision between traditional savings accounts and Certificates of Deposit (CDs) is more relevant than ever. Both options offer unique benefits and drawbacks, influenced by current economic conditions, interest rates, inflation, and your financial goals. This comprehensive guide will explore the nuances of savings accounts and CDs in 2026, helping you make an informed decision on where to store your money safely while maximizing returns.

Understanding Savings Accounts in 2026

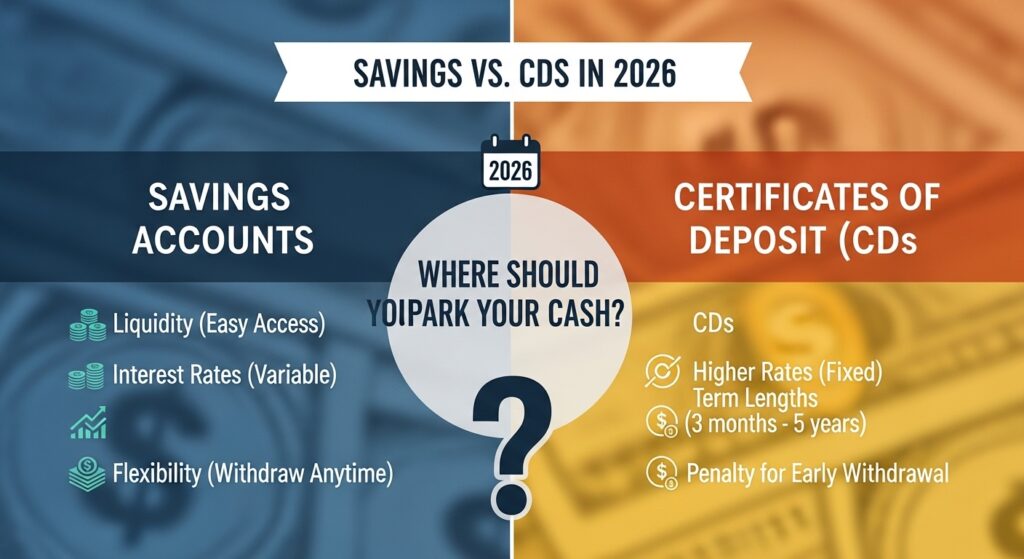

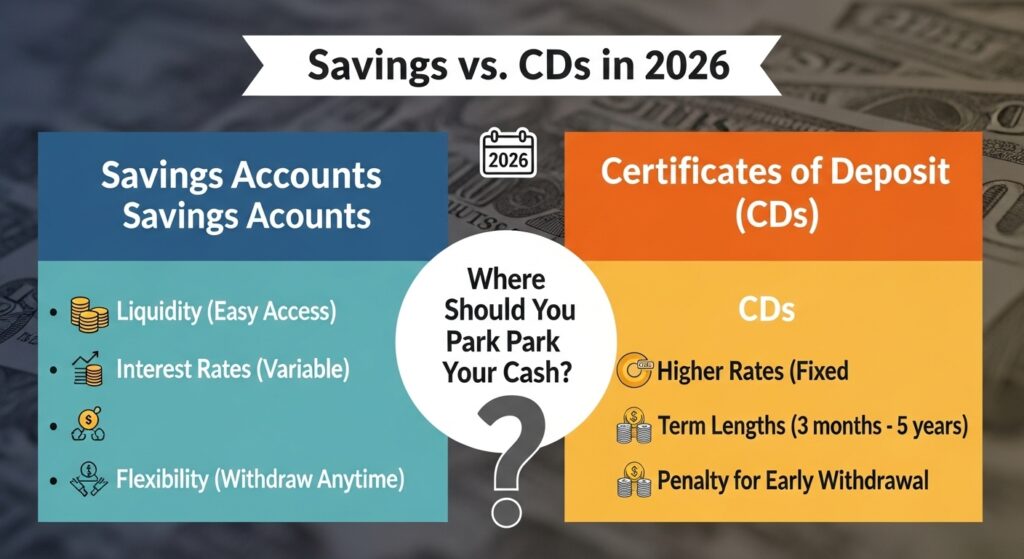

Savings accounts have long been the go-to option for individuals seeking liquidity and safety. They offer easy access to funds and typically come with minimal fees. In 2026, savings accounts continue to evolve with competitive interest rates driven by central bank policies and the rise of digital banking platforms.

Types of Savings Accounts

- Traditional Savings Accounts: Offered by most banks and credit unions, these accounts provide a safe place to hold money with modest interest rates. They are insured by the FDIC (Federal Deposit Insurance Corporation) or NCUA (National Credit Union Administration) up to $250,000, making them virtually risk-free.

- High-Yield Savings Accounts: Online banks and fintech companies have popularized high-yield savings accounts, which offer significantly higher interest rates than traditional savings accounts. These accounts often have fewer fees and require lower minimum balances.

- Money Market Accounts: These accounts blend features of savings and checking accounts, offering higher interest rates with limited check-writing capabilities.

Interest Rates and Inflation Impact

In 2026, interest rates on savings accounts have seen moderate increases compared to previous years, reflecting central banks’ responses to inflationary pressures. However, despite these rate hikes, many savings account yields still struggle to outpace inflation, meaning the real purchasing power of your money could erode over time if solely parked in these accounts.

Liquidity and Accessibility

One of the biggest advantages of savings accounts is liquidity. Funds can be accessed quickly through online transfers, ATM withdrawals, or branch visits. This makes savings accounts ideal for emergency funds or short-term financial goals.

Pros of Savings Accounts in 2026

- High liquidity with easy access to funds

- FDIC or NCUA insured, offering safety

- No or low minimum balance requirements

- Increasing availability of high-yield options through online banks

Cons of Savings Accounts in 2026

- Interest rates may not keep pace with inflation

- Lower returns compared to other investment vehicles

- Some accounts impose monthly withdrawal limits (usually six per month)

Understanding Certificates of Deposit (CDs) in 2026

Certificates of Deposit, or CDs, are time-bound deposits offered by banks and credit unions that typically provide higher interest rates than savings accounts in exchange for locking in your money for a fixed term. In 2026, CDs remain a popular choice for conservative investors seeking predictable returns.

Types of CDs

- Traditional CDs: Fixed interest rates for a set term ranging from a few months to several years. Early withdrawal usually incurs penalties.

- Bump-Up CDs: Allow you to increase your interest rate once during the term if rates rise.

- No-Penalty CDs: Provide the flexibility to withdraw funds early without penalties, though the interest rates might be slightly lower.

- Jumbo CDs: Require larger minimum deposits, often $100,000 or more, and offer higher interest rates.

Interest Rate Environment for CDs in 2026

With central banks adjusting rates to balance economic growth and inflation, CD rates in 2026 have seen a gradual increase. Longer-term CDs tend to offer better rates, but the risk of locking in money during fluctuating interest periods remains a consideration.

Liquidity and Early Withdrawal Penalties

The biggest trade-off with CDs is liquidity. Money is tied up for the duration of the term, and early withdrawals often result in penalties, which can eat into your principal or earned interest. However, no-penalty CDs provide an alternative with slightly reduced yields but greater flexibility.

Pros of CDs in 2026

- Higher interest rates compared to most savings accounts

- Predictable, fixed returns ideal for risk-averse investors

- FDIC or NCUA insured up to $250,000

- Variety of terms and structures to fit different investment horizons

Cons of CDs in 2026

- Reduced liquidity due to fixed term commitments

- Early withdrawal penalties can reduce returns

- Potential opportunity cost if interest rates rise after locking in a CD

Comparing Savings Accounts and CDs: Which One is Right for You?

When deciding between savings accounts and CDs in 2026, it’s essential to consider your financial goals, risk tolerance, and need for liquidity.

1. Purpose of Funds

- Emergency Fund: Savings accounts are generally better due to their liquidity and easy access.

- Short-Term Goals (under 1 year): Savings accounts or short-term CDs (3 to 6 months) can be suitable.

- Medium to Long-Term Goals (1+ years): CDs may provide higher returns and can be a good choice if you don’t need immediate access to funds.

2. Interest Rate Outlook

If interest rates are expected to rise, locking in a long-term CD might not be ideal as you could miss out on higher yields later. In such scenarios, a high-yield savings account or a no-penalty CD offers more flexibility.

3. Inflation Considerations

Neither savings accounts nor CDs typically beat inflation by a large margin, but CDs generally offer better rates. However, for long-term growth, consider diversifying into other investment options alongside your cash holdings.

4. Risk Tolerance

Both savings accounts and CDs are low-risk, insured options, but the liquidity risk of CDs should be factored in.

Strategies for Maximizing Returns on Cash in 2026

- Laddering CDs: Staggering CD maturity dates allows you to access portions of your cash periodically while benefiting from higher rates on longer terms.

- Utilizing High-Yield Savings Accounts: Online banks continue to offer competitive rates that can outperform traditional banks.

- Combining Products: Use a combination of savings accounts for liquidity and CDs for higher yields.

- Monitoring Rate Changes: Stay informed about Federal Reserve moves and adjust your cash holdings accordingly.

Tax Implications

Interest earned on both savings accounts and CDs is taxable as ordinary income. Consider tax-advantaged accounts like IRAs if you want to shelter your interest earnings.

Future Outlook: Savings and CDs Beyond 2026

As technology advances and financial products evolve, expect more innovative cash management tools. Digital banks and fintech platforms may continue to disrupt traditional savings and CD offerings, potentially providing better rates and more flexible terms.

Conclusion

In 2026, the choice between savings accounts and CDs depends largely on your personal financial situation, goals, and the current economic environment. Savings accounts offer unmatched liquidity and safety, making them suitable for emergency funds and short-term savings. CDs, on the other hand, provide higher, fixed returns for those willing to lock in their money for a set period.

By understanding the pros and cons of each option, considering interest rate trends, and aligning choices with your financial objectives, you can effectively park your cash to maximize safety and returns. Remember, diversifying your cash holdings across different instruments may be the best strategy to balance liquidity and growth in an uncertain economic landscape.

Start by evaluating your needs today and explore the latest offerings from banks and credit unions to find the savings account or CD that best fits your financial goals in 2026.