Why Every 20-Year-Old Needs a High-Yield Savings Account Now: If you are 20 years old in 2026, you are likely navigating the most complex financial landscape in decades. Between the rise of gig-economy work, the integration of AI in every career path, and the reality of 2.4% inflation, the “traditional” advice of just saving your pennies isn’t enough.

The move from a standard savings account to a High-Yield Savings Account (HYSA) is no longer a “pro tip”—it is a mathematical necessity for your survival and success.

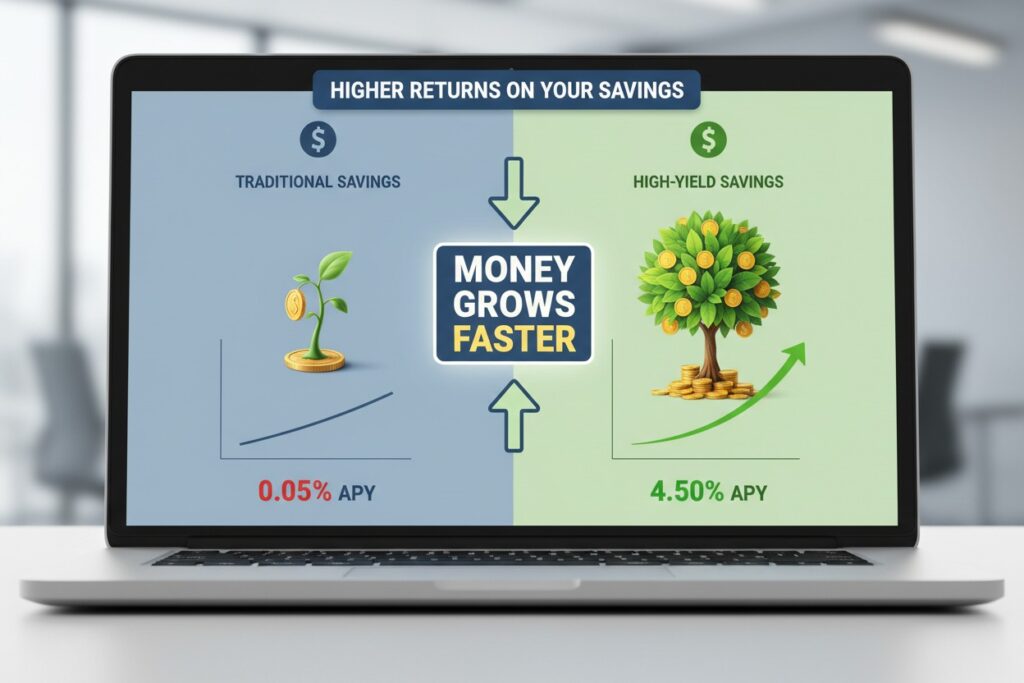

1. The “10x” Reality Check: 0.39% vs. 4.20%

In March 2026, the national average interest rate for a standard savings account at a “Big Four” bank is a staggering 0.39%. Meanwhile, top-tier HYSAs are offering 4.00% to 4.20%.

The Math of Your Money:

If you save $5,000 for a future house deposit or car:

- Standard Account (0.39%): You earn $19.50 in a year.

- High-Yield Account (4.20%): You earn $210.00 in a year.

By simply moving your money to a different digital vault, you earn nearly $200 for doing zero work. For a 20-year-old, that’s a free flight, a new pair of tech-specs, or several months of groceries.

2. Fighting the “Inflation Stealth Tax”

Inflation in 2026 is currently hovering around 2.4%. If your money is in a standard account earning 0.39%, you are effectively losing 2% of your wealth every year because the prices of goods are rising faster than your bank is paying you.

An HYSA at 4%+ is your only “safe” way to ensure your money actually gains purchasing power while you sleep. It turns your savings from a shrinking pile into a growing asset.

3. The “Financial Runway” for a Gig Economy

The job market in 2026 is highly specialized. Whether you are a content creator, a developer, or a student, your income may not always be a steady paycheck. An HYSA serves as your Financial Runway.

- The Goal: Build a $2,000 “Starter Emergency Fund.”

- The Benefit: Having this money in an HYSA means that if your laptop breaks or your car needs a sensor replacement, you aren’t forced to use a high-interest credit card (which in 2026 can have rates as high as 29%).

4. Compound Interest: Your Only “Unfair” Advantage

At 20, your greatest asset isn’t your degree or your job—it’s time.

If you start with $1,000 and add $100 a month into a 4.2% HYSA:

- In 5 years (Age 25): You have $7,900.

- In 10 years (Age 30): You have $16,500.

Because you are earning “interest on your interest,” the longer you leave the money in a high-rate environment, the faster the “snowball” rolls. If you wait until you are 30 to start, you would have to save twice as much per month to catch up to where you would have been if you started at 20.

5. Top 3 “Zero-Barrier” HYSAs for 20-Year-Olds in 2026

| Bank | APY (March 2026) | Minimum Balance | Why it’s Great |

| LendingClub | 4.00% | $0 | The “Set and Forget” winner. |

| SoFi | 4.20% | $0 | Best all-in-one app with “Vaults” for goals. |

| Capital One 360 | 3.70% | $0 | Best if you occasionally want a physical location. |

Conclusion: Don’t Leave Money on the Table

Starting your financial journey at 20 is about building habits. Opening an HYSA takes less than 10 minutes on your phone and immediately puts you in the top 10% of financially literate young adults. You are essentially giving yourself a “raise” without having to ask a boss for one.