In early 2026, the global interest rates landscape is undergoing a “bumpy” shift. After a period of cooling in late 2024 and 2025, central banks like the RBA and the Bank of England have recently signaled a pivot back toward caution—and in some cases, rate hikes—due to stubborn inflation in services and housing.

Understanding why these rates are moving is the first step toward making sure they don’t derail your financial goals.

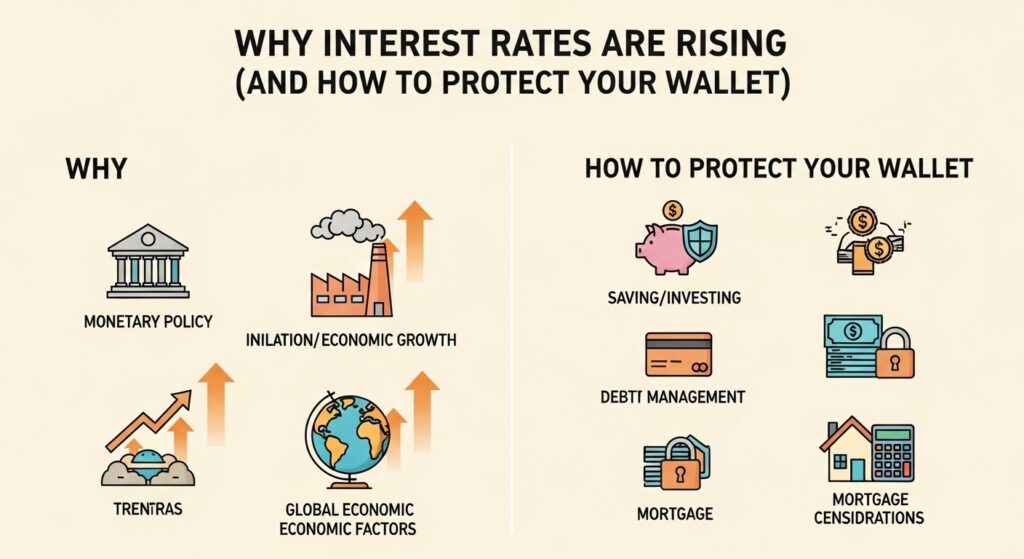

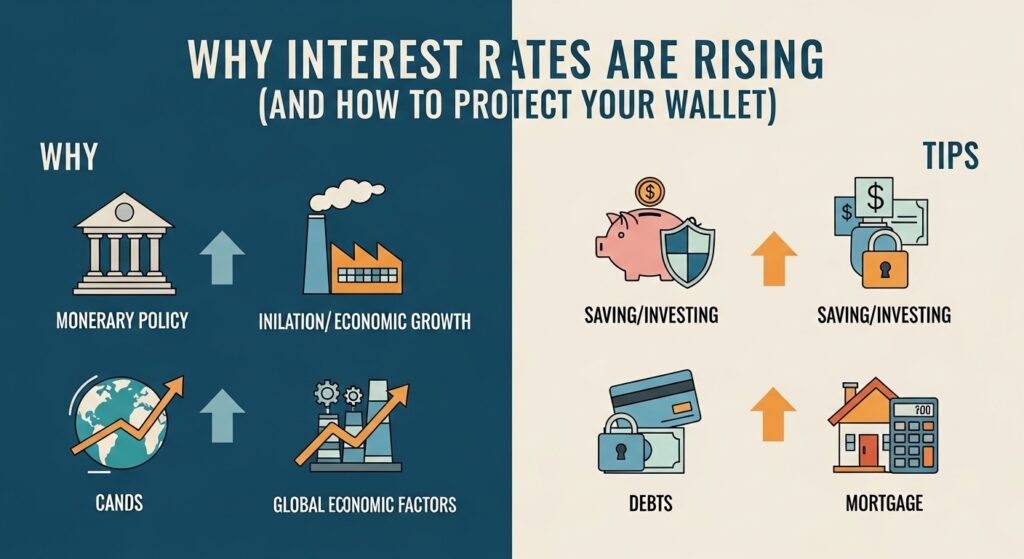

Why Rates are Rising (or Staying High) in 2026

Interest rates are essentially the “cost of money.” When inflation stays above the 2% target, central banks raise rates to discourage spending, which cools down prices. Currently, several factors are keeping that pressure alive:

- Service Sector Inflation: While the cost of physical goods has stabilized, the prices for services—like dining out, travel, and healthcare—have remained high due to strong consumer demand.

- Housing Market Resilience: Despite higher rates, housing prices in many regions have continued to climb, fueled by tight inventory. This “wealth effect” keeps people spending, forcing banks to keep rates restrictive.

- Labor Market Tightness: Unemployment remains near historic lows (around 4.25% – 4.5%). When more jobs are available than workers to fill them, wages rise, which can further fuel inflation.

- Fiscal Expansion: Significant government spending and tax policy changes in late 2025 have injected fresh cash into the economy, complicating the Federal Reserve’s path to lower rates.

How to Protect Your Wallet

Rising rates aren’t all bad news, but they do require a change in strategy. Here is how to position yourself in the current environment:

1. Pivot Your Debt Strategy

If you have variable-rate debt (like a credit card or an ARM), you are most at risk.

- Consolidate Now: If you have high-interest credit card debt, look for a 0% intro APR balance transfer card. These are becoming rarer as rates rise, so acting sooner is better.

- Lock in Fixed Rates: If you are shopping for a mortgage, today’s rates (averaging around 6.24% for a 30-year fixed as of February 2026) are lower than they were a year ago but likely to stay “higher for longer.” Consider a 15-year fixed if your budget allows to save on total interest.

2. Maximize Your Savings (The Silver Lining)

The one group that wins when rates rise? Savers. * Ditch Your Big Bank: Traditional “big” banks often offer 0.01% on savings. High-Yield Savings Accounts (HYSAs) and CDs in 2026 are still offering competitive returns.

- CD Ladders: If you think rates have peaked, “lock in” current yields by opening a CD ladder. This involves splitting your savings into CDs that mature at different intervals (6 months, 1 year, 2 years).

3. Review Your Investment Mix

- Fixed Income: Shorter-duration bonds (5–7 years) are currently preferred by analysts to manage risk while taking advantage of elevated yields.

- Real Assets: Inflation-sensitive assets like real estate or infrastructure can act as a hedge if prices continue to rise.

4. “Stress Test” Your Budget

Perform a “What-If” analysis. If your mortgage or rent were to increase by another 0.5% – 1%, would your current lifestyle be sustainable? Increasing your emergency fund to cover 6 months of expenses is the best defense against economic uncertainty.